Texas generated 30% of its electricity last year with carbon-free resources (mostly wind.) Coals has shrunk over the last decade from 37% to 25%.

Texas generated 30% of its electricity last year with carbon-free resources (mostly wind.) Coals has shrunk over the last decade from 37% to 25%.

PG&E spends $275 million a year on energy efficiency investments that reduce demand by 100 MW. It also spends $65 million a year on demand response to reduce peak loads by 400 MW. If we assume that energy efficiency investments are effective an average of 12 years the incremental cost of those investments is $66 per MWH (6.6 cents per kWh). For demand response the incremental cost, which should match the market value, is $163 per kilowatt-year (or $13.60 per kW-month). Both of these values are reasonable investments for long-term resources.

Yet, PG&E argues in the PCIA exit fee proceeding and its annual ERRA generation cost proceeding that the appropriate market valuation for its resources are the short-term fire sale values that it realizes in the daily markets. According to PG&E, customers do not realize any additional value from holding these resources beyond what those resources can be bought and sold for the CAISO markets and in bilateral short-term deals.

So we are left with the obvious question: Why is PG&E continuing to invest in energy efficiency and demand response if the utility states that it can meet all of its needs in the short-term markets? This hypocrisy is probably best explained by PG&E manipulating the regulatory process. PG&E’s proposed “market valuation” sets the exit fee for community choice aggregation (CCA) at a high level. Instead, that market valuation should reflect how much CCAs have saved bundled customers in avoided procurement, and what PG&E pays for adding new resources.

Kevin Novan from UC Davis wrote an article in the University of California Giannini Foundation’s Agriculture and Resource Economics Update entitled “Should Communities Get into the Power Marketing Business?” Novan was skeptical of the gains from community choice aggregation (CCA), concluding that continued centrally planned procurement was preferable. Other UC-affiliated energy economists have also expressed skepticism, including Catherine Wolfram, Severin Borenstein, and Maximilian Auffhammer.

At the heart of this issue is the question of whether the gains of “perfect” coordination outweigh the losses from rent-seeking and increased risks from centralized decision making. I don’t consider myself an Austrian economist, but I’m becoming a fan of the principle that the overall outcomes of many decentralized decisions is likely to be better than a single “all eggs in one basket” decision. We pretend that the “central” planner is somehow omniscient and prudently minimizes risks. But after three decades of regulatory practice, I see that the regulators are not particularly competent at choosing the best course of action and have difficulty understanding key concepts in risk mitigation.By distributing decision making, we better capture a range of risk tolerances and bring more information to the market place. There are further social gains from dispersed political decision making that brings accountability much closer to home and increases transparency. Of course, there’s a limit on how far decentralization should go–each household can’t effectively negotiate separate power contracts. But we gain much more information by adding a number of generation service providers or “load serving entities” (LSE) to the market.

I found several shortcomings with with Novan’s article that would change the tenor. I take each in turn:

I was on the City of Davis Community Choice Energy Advisory Committee, and I am testifying on behalf of the California CCAs on the setting of the PCIA in several dockets. I have a Ph.D. from Berkeley’s ARE program and have worked on energy, environmental and water issues for about 30 years.

As I listen to the opening of the joint California Customer Choice En Banc held by the CPUC and CEC, I hear Commissioners and speakers claiming that community choice aggregators (CCAs) are taking advantage of the current market and shirking their responsibilities for developing a responsible, resilient resource portfolio.

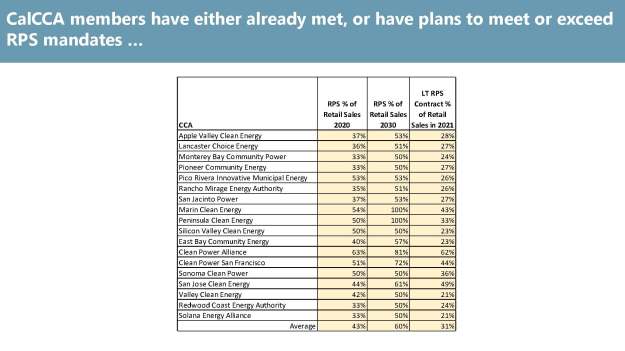

The CPUC’s view has two problems. The first is an unreasonable expectation that CCAs can start immediately as a full-grown organization with a complete procurement organization, and more importantly, a rock solid credit history. The second is how the CPUC has ignored the fact that the CCAs have already surpassed the state’s RPS targets in most cases and that they have significant shares of long-term power purchase agreements (PPAs).

State law in fact penalizes excess procurement of RPS-eligible power by requiring that 65% of that specific portfolio be locked into long-term PPAs, regardless of the prudency of that policy. PG&E has already demonstrated that they have been unable to prudently manage its long-term portfolio, incurring a 3.3 cents per kilowatt-hour risk hedge premium on its RPS portfolio. (Admittedly, that provision could be interpreted to be 65% of the RPS target, e.g., 21.5% of a portfolio that has met the 33% RPS target, but that is not clear from the statute.)

Nick Chaset is the CEO of East Bay Community Energy which is a community choice aggregator (CCA) that serves Alameda County. He also was Commission President Michael Picker’s chief advisor until last year when he left for EBCE. He explains in this article how two proposed decisions that the CPUC is considering are fundamentally wrong and will shift cost onto CCA customers. (I testified on behalf of CalCCA in this proceeding. I’ll have more on this before the Commission’s scheduled vote October 11.)

Figure 1 – CPUC’s Proposed Resource Adequacy Value vs. True Market Values

Figure 2 – GHG Premium Value Missing from CPUC Proposed Decision

Figure 3 – Falling Utility Rates as Customers Depart Filed in Their ERRA Rate Applications

I received a notice of a new MIT study entitled “The Future of Nuclear Energy in a Carbon-Constrained World” which looks at the technological, regulatory and economic changes required to make nuclear power viable again. A summary states

The findings are that new policy models and cost-cutting technologies would help nuclear play vital role in climate solutions. Progress in reducing carbon emissions requires a broad range of actions to effectively leverage nuclear energy.

However, nothing in the summary reveals the paradigm-shattering innovation that will be required to make nuclear power competitive with a diverse fleet of renewables plus storage that would achieve the same goals. The cost of a solar plant plus storage with today’s technology still costs less than a current technology nuclear plant. That alternative fleet would also provide better reliability by diversifying the generation sources through smaller plants and avoid any radiation contamination risk.

The nuclear industry must clearly demonstrate that it can get past the many hurdles that led to the recent cancellation of two projects in the southeast U.S. Reviving nuclear power will require more than fantasies about what might be.

![]()

Valley Clean Energy Alliance (VCE) was in the Davis opinion columns this weekend again. First, Bob Dunning wrote another column in the Davis Enterprise that mischaracterizes the switch to VCE from PG&E as “mandated” and implies that local government didn’t trust Davis citizens to make the right choice. Then, David Greenwald wrote a column in the Davis Vanguard on how Dunning had ignored the authorization of the development and formation of VCE and is late to the game.

In both cases, the distinction between the choice to form VCE made by city councils and the Board of Supervisors after substantial study is not distinguished from the choice that electricity ratepayers now have as to which entity will serve them. Previously, Yolo County ratepapers had no choice as to who should serve them–it took the formation of VCE to create that choice. If Dunning has a problem with that even offering that choice in the first place, then that’s a much more fundamental problem. But he is not being so transparent in his opposition, with is either disingenuous or ignorant.

I wrote the following email to Bob Dunning (I had an earlier letter to the editor already published in the Enterprise, that I also posted on this blog and the Davis Vanguard.)

You complain that somehow you’ve been “mandated” to sign up with Valley Clean Energy Authority. Yet you fail to ask the question “why was I mandated to sign up with PG&E all of those years?” Why does PG&E get a free pass from your scrutiny?

Instead now, you actually have a choice. We trust that you will make the right choice, whereas before you had NO choice. And you are not “mandated” to join VCE. You can act to switch to PG&E if you so choose. What has changed is the starting point of your choice. The default is no longer PG&E—it’s VCE. There’s nothing wrong with changing the default choice, but we have to start with a default since everyone wants to continue to receive electricity. (The other option is like they did with long distance service in the late 1980s with random assignment as the starting point, but that seems too much bother.)

Send me your answers in your next column.

As to the Vanguard, I posted:

I think your column misses the fundamental point–contrary to everything that Dunning writes, we DO have a choice–it’s just that the starting point (default) isn’t what he wants. He prefers that the big corporations get the favored pole position.

The California Legislature is considering a bill (AB 893) that would require the state’s regulated utilities (including CCAs as well as investor-owned) to buy at least 4,250 megawatts of renewables before federal tax credits expire in 2022.

Unfortunately, this will not create the cost savings that seem so obvious. This argument was made by the renewable energy plant owners in the Diablo Canyon Power Plant retirement case (A.16-08-006) and rejected by the CPUC in its decision. While the tax credits lower current costs, these are more than offset by waiting for technology costs to fall even further, as shown by the solar power forecast above. Combined with the time value of money (discounting), the value of waiting far outweighs prematurely buying renewables.

The legislature already passed a bill (SB 1090) that requires the CPUC to ensure that GHG emissions will not rise when Diablo Canyon retires in 2024 and 2025 when approving integrated resource plans. (Whether the governor signs this overly directive law is another question.) And SB 100 requires reaching 100% carbon free by 2045. A study just released by the Energy Institute at Haas indicates that renewables to date have depressed energy market prices, discouraging further investment. And the CAISO is “managing oversupply” created by the current renewable generation.

And there’s a further problem–with a large number of customers moving from the IOUs to CCAs across all three utilities, the question is “who should be responsible for buying this power?” The CCAs will have their own preferences (often locally and community-scale) that will conflict with any choices made by the IOUs. The CCAs are already saddled with poor procurement and portfolio management decisions by the IOUs through exit fees. (PG&E has an embedded risk premium of $33 per megawatt-hour in its RPS portfolio costs.) Why would we want the IOUs to continue to mismanage our power resources?

The California Legislature is still struggling with whether and how it should protect PG&E from a $17 billion liability from the Sonoma wildfires that could push the utility into bankruptcy. The latest proposal would have the CPUC conduct a “stress test” on PG&E’s finances if it faced a large liability, and then PG&E could raise rates sufficiently to cover the difference between the total liability and exposure deemed sufficient to maintain financial solvency. We don’t have enough details to understand how well the stress threshold is defined and how it would differ from the current cost of capital evaluations, but this is a bad idea regardless.

Firms need the threat of bankruptcy to perform efficiently and effectively. We’ve already seen how PG&E manages and performs sloppily, whether its maintaining vegetation (which has been a problem since the early 1990s), tracking its pipeline maintenance (which led to the San Bruno accident), or managing risk in its renewable power portfolio (which has added a $33 per megawatt-hour premium to its cost.) Clearly CPUC oversight alone is not doing the job. Outside litigation may be the only way to get PG&E’s attention, especially if it creates an existential threat.

Policymakers have taken the wrong lesson from PG&E’s previous bankruptcy, filed in 2001 during the California energy crisis. The issue there that lead to the final resolution was whether PG&E was required to provide power to its customers at whatever cost. This situation is not about PG&E’s obligations but rather about its management practices, and a bankruptcy court is much less likely to require a cost pass through.

Instead, the state could simply step in buy PG&E for $1 if the utility declares bankruptcy (an option that Governor Gray Davis was too much of a coward to consider in March 2001.) The state could then directly manage the utility, or better yet, parse it down to eight or ten smaller utilities. (Two studies in PG&E’s 1999 General Rate Case, and the subsequent decision, found that the most efficient utility size is about 500,000 customers. PG&E now has over four million.) Customers would find the utilities more accessible and responsive, and by creating municipal utilities, rates could be much lower with cheaper financing cost. It’s time to rethink where we should head.

Severin Borenstein at UC Berkeley argues against the “try everything” approach to searching for solutions to mitigating greenhouse gas emissions. But he is confusing situations with relatively small incremental consequences (even the California WaterFix is “small” compared to potential climate change impacts.)

Instead, when facing a potentially large catastrophic outcome for which the probability distribution is completely unknown, we need a different analytic approach than a simple cost-benefit analysis based on an “expected” outcome.

We need to be looking for what decision pathways lead us to the situations create the most vulnerability, not for which one has the “optimal outcome.” Policymakers and stakeholders looking desperately for any solution intuitively get the notion of robust decisionmaking, but are not receiving much guidance about how to best pursue this alternative approach. Economists need to lead the conversation that changes the current misleading perspective.

All Things Solar and Electric

Musings from M.Cubed on the environment, energy and water

This blog is not necessarily about biking. It's about life that is lived locally, at a human pace.

Energy, Environment and Policy

Musings from M.Cubed on the environment, energy and water

Examining State Authority in Interstate Electricity Markets

Musings from M.Cubed on the environment, energy and water

Musings from M.Cubed on the environment, energy and water

Economic insight and analysis from The Wall Street Journal.

Musings from M.Cubed on the environment, energy and water

Musings from M.Cubed on the environment, energy and water

A few thoughts from John Fleck, a writer of journalism and other things, living in New Mexico

Musings from M.Cubed on the environment, energy and water

Musings from M.Cubed on the environment, energy and water

Musings from M.Cubed on the environment, energy and water

Tips and tricks on programming, evolutionary algorithms, and doing research

Musings from M.Cubed on the environment, energy and water

A blog about water resources and law

Musings from M.Cubed on the environment, energy and water