Severin Borenstein at the Energy Institute at Haas has written another blog post asserting that solar rooftop rates are inefficient and must changed radically. (I previously responded to an earlier post.) When looking at the efficiency of NEM rates, we need to look carefully at several elements of electricity market and the overall efficiency of utility ratemaking. We can see that we can come to a very different conclusion.

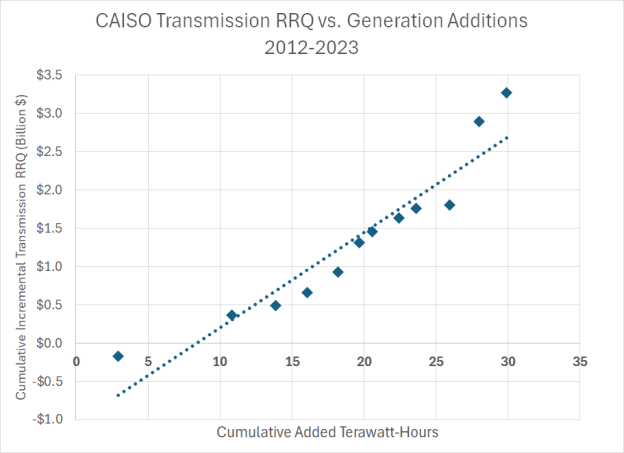

I filed testimony in the NEM 3.0 rulemaking last month where I calculated the incremental cost of transmission investment for new generation and the reduction in the CAISO peak load that looks to be attributable to solar rooftop.

- Using FERC Form 1 and CEC powerplant data, I calculated that the incremental cost of transmission is $37/MWH. (And this is conservative due to a couple of assumptions I made.) Interestingly, I had done a similar calculation for AEP in the PJM interconnect and also came up with $37/MWH. This seems to be a robust value in the right neighborhood.

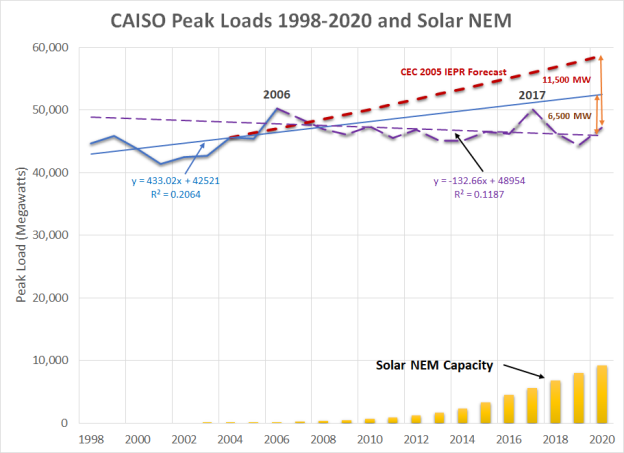

- Load growth in California took a distinct change in trend in 2006 just as solar rooftop installations gained momentum. I found a 0.93 correlation between this change in trend and the amount of rooftop capacity installed. Using a simple trend, I calculated that the CAISO load decreased 6,000 MW with installation of 9,000 MW of rooftop solar. Looking at the 2005 CEC IEPR forecast, the peak reduction could be as large as 11,000 MW. CAISO also estimated in 2018 that rooftop solar displaced in $2.6 billion in transmission investment.

When we look at the utilities’ cost to acquire renewables and add in the cost of transmission, we see that the claim that grid-scale solar is so much cheaper than residential rooftop isn’t valid. The “green” market price benchmark used to set the PCIA shows that the average new RPS contract price in 2016 was still $92/MWH in 2016 and $74/MWH in 2017. These prices generally were for 30 year contracts, so the appropriate metric for comparing a NEM investment is against the vintage of RPS contracts signed in the year the rooftop project was installed. For 2016, adding in the transmission cost of $37/MWH, the comparable value is $129/MWH and in 2017, $111/MWH. In 2016, the average retail rates were $149/MWH for SCE, $183/MWH for PG&E and $205/MWH for SDG&E. (Note that PG&E’s rate had jumped $20/MWH in 2 years, while SCE’s had fallen $20/MWH.) In a “rough justice” way, the value of the displaced energy via rooftop solar was comparable to the retail rates which reflect the value of power to a customer, at least for NEM 1.0 and 2.0 customers. Rooftop solar was not “multiples” of grid scale solar.

These customers also took on investment risk. I calculated the payback period for a couple of customers around 2016 and found that a positive payback was dependent on utility rates rising at least 3% a year. This was not a foregone conclusion at the time because retail rates had actually be falling up to 2013 and new RPS contract prices were falling as well. No one was proposing to guarantee that these customers recover their investments if they made a mistake. That they are now instead benefiting is unwarranted hubris that ignores the flip side of the importance of investment risk–that investors who make a good efficient decision should reap the benefits. (We can discuss whether the magnitude of those benefits are fully warranted, but that’s a different one about distribution of income and wealth, not efficiency.)

Claiming that grid costs are fixed immutable amount simply isn’t a valid claim. SCE has been trying unsuccessfully to enact a “grid charge” with this claim since at least 2006. The intervening parties have successfully shown that grid costs in fact are responsive to reductions in demand. In addition, moving to a grid charge that creates a “ratchet effect” in revenue requirements where once a utility puts infrastructure in place, it faces no risk for poor investment decisions. On the other hand the utility can place its costs into ratebase and raise rates, which then raises the ratchet level on the fixed charge. One of the most important elements of a market economy that leads to efficient investment is that investors face the risk of not earning a return on an investment. That forces them to make prudent decisions. A “ratcheted” grid charge removes this risk even further for utilities. If we’re claiming that we are creating an “efficient” pricing policy, then we need to consider all sides of the equation.

The point that 50% of rooftop solar generation is used to offset internal use is important–while it may not be exactly like energy efficiency, it does have the most critical element of energy efficiency. That there are additional requirements to implement this is of second order importance, Otherwise we would think of demand response that uses dispatch controls as similarly distinct from EE. Those programs also require additional equipment and different rates. But in fact we sum those energy savings with LED bulbs and refrigerators.

An important element of the remaining 50% that is exported is that almost all of it is absorbed by neighboring houses and businesses on the same local circuit. Little of the power goes past the transformer at the top of the circuit. The primary voltage and transmission systems are largely unused. The excess capacity that remains on the system is now available for other customers to use. Whether investors should be able to recover their investment at the same annual rate in the face of excess capacity is an important question–in a competitive industry, the effective recovery rate would slow.

Finally, public purpose program (PPP) and wildfire mitigation costs are special cases that can be simply rolled up with other utility costs.

- The majority of PPP charges are a form of a tax intended for income redistribution. That function is admirable, but it shows the standard problem of relying on a form of a sales tax to finance such programs. A sales tax discourages purchases which then reduces the revenues available for income transfers, which then forces an increase in the sales tax. It’s time to stop financing the CARE and FERA programs from utility rates.

- Wildfire costs are created by a very specific subclass of customers who live in certain rural and wildlands-urban interface (WUI) areas. Those customers already received largely subsidized line extensions to install service and now we are unwilling to charge them the full cost of protecting their buildings. Once the state made the decision to socialize those costs instead, the costs became the responsibility of everyone, not just electricity customers. That means that these costs should be financed through taxes, not rates.

Again, if we are trying to make efficient policy, we need to look at the whole. It is is inefficient to finance these public costs through rates and it is incorrect to assert that there is an inefficient subsidy created if a set of customers are avoiding paying these rate components.