The saying goes “No good deed goes unpunished.” The California Public Utilities Commission seems to have taken that motto to heart recently, and stands ready to penalize yet another group of customers who answered the clarion call to help solve the state’s problems by radically altering the rules for solar rooftops. Here’s three case studies of recent CPUC actions that undermine incentives for customers to act in the future in response to state initiatives: (1) farmers who invested in response to price incentives, (2) communities that pursued renewables more assertively, and (3) customers who installed solar panels.

Agriculture: Farmers have responded to past time of use (TOU) rate incentives more consistently and enthusiastically than any other customer class. Instead of being rewarded for their consistency, their peak price periods shifted from the afternoon to the early evening. Growers face much more difficulty in avoiding pumping during that latter period.

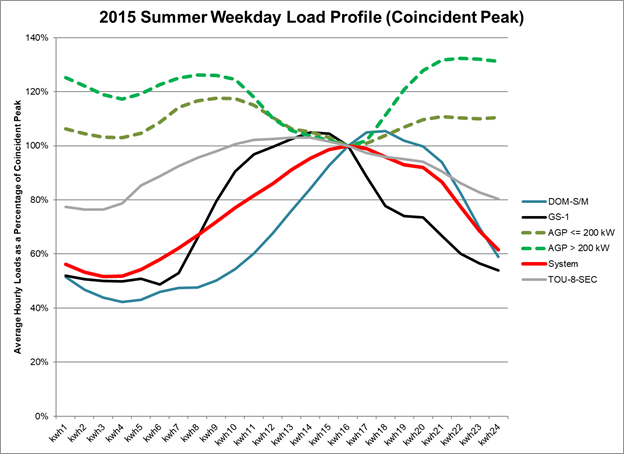

Since TOU rates were introduced to agricultural customers in the late 1970s, growers have made significant operational changes in response to TOU differentials between peak and off-peak energy prices to minimize their on-peak consumption. These include significant investments in irrigation equipment, storage and conveyance infrastructure and labor deployment rescheduling. The results of these expenditures are illustrated in the figure below, which shows how agricultural loads compare with system-wide load on a peak summer weekday in 2015, contrasting hourly loads to the load at the coincident peak hour. Both the smaller and larger agricultural accounts perform better than a range of representative rate schedules. Most notably agriculture’s aggregate load shape on a summer weekday is inverted relative to system peak, i.e., the highest agricultural loads occur during the lowest system load periods, in contrast with other rate classes.

All other rate schedules shown in the graphic hit their annual peak on the same peak day within the then-applicable peak hours of noon to 6 p.m. In contrast, agriculture electricity demand is less than 80% of its annual peak during those high-load hours, with its daily peak falling outside the peak period. Agriculture’s avoidance of peak hours occurred during the summer agricultural growing season, which coincided with peak system demand—just as the Commission asked customers to do. The Commission could not ask for a better aggregate response to system needs; in contrast to the profiles for all of the other customer groups, agriculture has significantly contributed to shifting the peak to a lower cost evening period.

The significant changes in the peak period price timing and differential that the CPUC adopted increases uncertainty over whether large investments in high water-use efficiency microdrip systems – which typically cost $2,000 per acre–will be financially viable. Microdrip systems have been adopted widely by growers over the last several years—one recent study of tomato irrigation rates in Fresno County could not find any significant quantity of other types of irrigation systems. Such systems can be subject to blockages and leaks that are only detectable at start up in daylight. Growers were able to start overnight irrigation at 6 p.m. under the legacy TOU periods and avoid peak energy use. In addition, workers are able to end their day shortly after 6 p.m. and avoid nighttime accidents. Shifting that load out of the peak period will be much more difficult to do with the peak period ending after sunset.

Contrary to strong Commission direction to incent customers to avoid peak power usage, the shift in TOU periods has served to penalize, and reverse, the great strides the agricultural class has made benefiting the utility system over the last four decades.

Community choice aggregators: CCAs were created, among other reasons, to develop more renewable or “green” power. The state achieved its 2020 target of 33% in large part because of the efforts of CCAs fostered through offerings of 50% and 100% green power to retail customers. CCAs also have offered a range of innovative programs that go beyond the offerings of PG&E, SCE and SDG&E.

Nevertheless, the difficulty of reaching clean energy goals is created by the current structure of the PCIA. The PCIA varies inversely with the market prices in the market–as market prices rise, the PCIA charged to CCAs and direct access (DA) customers decreases. For these customers, their overall retail rate is largely hedged against variation and risk through this inverse relationship.

The portfolios of the incumbent utilities are dominated by long-term contracts with renewables and capital-intensive utility-owned generation. For example, PG&E is paying a risk premium of nearly 2 cents per kilowatt-hour for its investment in these resources. These portfolios are largely impervious to market price swings now, but at a significant cost. The PCIA passes along this hedge through the PCIA to CCAs and DA customers which discourages those latter customers from making their own long term investments. (I wrote earlier about how this mechanism discouraged investment in new capacity for reliability purposes to provide resource adequacy.)

The legacy utilities are not in a position to acquire new renewables–they are forecasting falling loads and decreasing customers as CCAs grow. So the state cannot look to those utilities to meet California’s ambitious goals–it must incentivize CCAs with that task. The CCAs are already game, with many of them offering much more aggressive “green power” options to their customers than PG&E, SCE or SDG&E.

But CCAs place themselves at greater financial risk under the current rules if they sign more long-term contracts. If market prices fall, they must bear the risk of overpaying for both the legacy utility’s portfolio and their own.

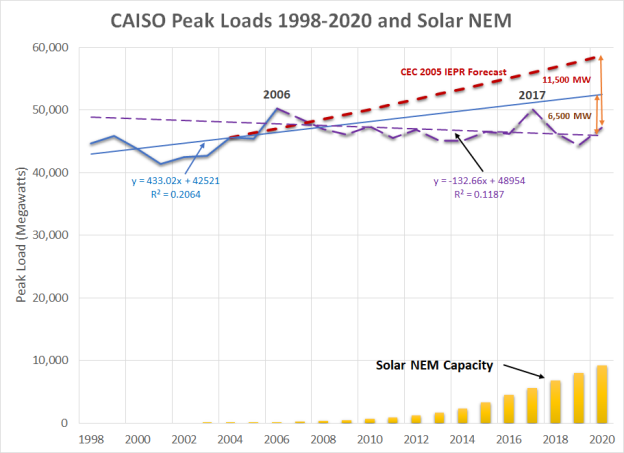

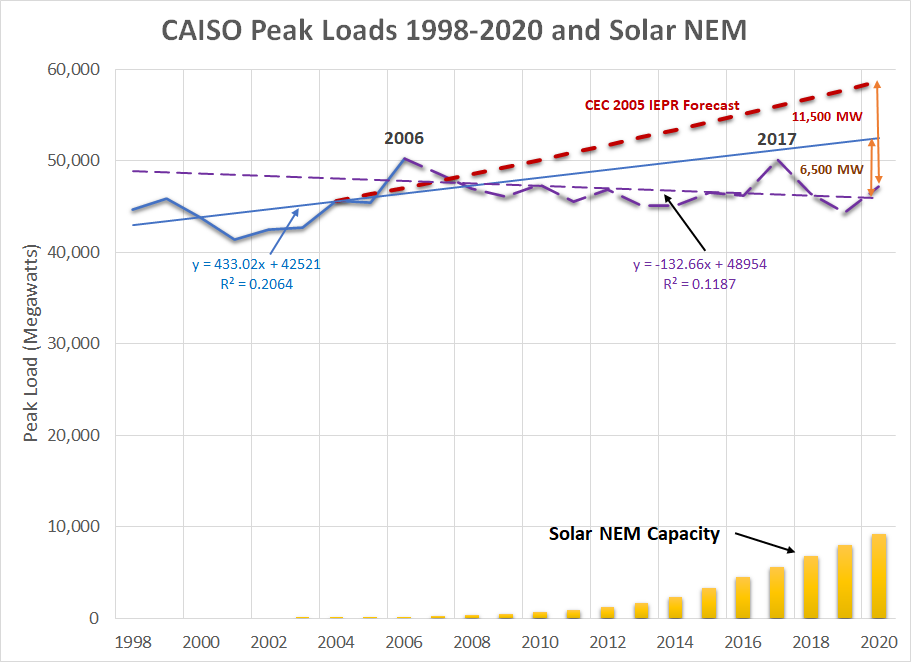

Solar net energy metered customers: Distributed solar generation installed under California’s net energy metering (NEM/NEMA) programs has mitigated and even eliminated load and demand growth in areas with established customers. This benefit supports protecting the investments that have been made by existing NEM/NEMA customers. Similarly, NEM/NEMA customers can displace investment in distribution assets. That distribution planners are not considering this impact appropriately is not an excuse for failing to value this benefit. For example, PG&E’s sales fell by 5% from 2010 to 2018 and other utilities had similar declines. Peak loads in the CAISO balancing authority reach their highest point in 2006 and the peak in August 2020 was 6% below that level.

Much of that decrease appears to have been driven by the installation of rooftop solar. The figure above illustrates the trends in CAISO peak loads in the set of top lines and the relationship to added NEM/NEMA installations in the lower corner. It also shows the CEC’s forecast from its 2005 Integrated Energy Policy Report as the top line. Prior to 2006, the CAISO peak was growing at annual rate of 0.97%; after 2006, peak loads have declined at a 0.28% trend. Over the same period, solar NEM capacity grew by over 9,200 megawatts. The correlation factor or “R-squared” between the decline in peak load after 2006 and the incremental NEM additions is 0.93, with 1.0 being perfect correlation. Based on these calculations, NEM capacity has deferred 6,500 megawatts of capacity additions over this period. Comparing the “extreme” 2020 peak to the average conditions load forecast from 2005, the load reduction is over 11,500 megawatts. The obvious conclusion is that these investments by NEM customers have saved all ratepayers both reliability and energy costs while delivering zero-carbon energy.

The CPUC now has before it a rulemaking in which the utilities and some ratepayer advocates are proposing to not only radically reduce the compensation to new NEM/NEMA customers but also to change the terms of the agreements for existing ones.

One of the key principles of providing financial stability is setting prices and rates for long-lived assets such as solar panels and generation plants at the economic value when the investment decision was made to reflect the full value of the assets that would have been acquired otherwise. If that new resource had not been built, either a ratebased generation asset would have been constructed by the utility at a cost that would have been recovered over a standard 30-year period or more likely, additional PPAs would have been signed. Additionally, the utilities’ investments and procurement costs are not subject to retroactive ratemaking under the rule prohibiting such ratemaking and Public Utilities Code Section 728, thus protecting shareholders from any risk of future changes in state or Commission policies.

Utility customers who similarly invest in generation should be afforded at least the same assurances as the utilities with respect to protection from future Commission decisions that may diminish the value of those investments. Moreover, customers do not have the additional assurances of achieving a certain net income so they already face higher risks than utility shareholders for their investments.

Generators are almost universally afforded the ability to recover capital investments based on prices set for multiple years, and often the economic life of their assets. Utilities are able to put investments in ratebase to be recovered at a fixed rate of return plus depreciation over several decades. Third-party generators are able to sign fixed price contracts for 10, 20, and even 40 years. Some merchant generators may choose to sell only into the short-term “hourly” market, but those plants are not committed to selling whenever the CAISO demands so. Generators are only required to do so when they sign a PPA with an assured payment toward investment recovery.

Ratepayers who make investments that benefit all ratepayers over the long term should be offered tariffs that provide a reasonable assurance of recovery of those investments, similar to the PPAs offered to generators. Ratepayers should be able to gain the same assurances as generators who sign long-term PPAs, or even utilities that ratebase their generation assets, that they will not be forced to bear all of the risk of investing of clean self-generation. These ratepayers should have some assurance over the 20-plus year expected life of their generation investment.