CCAs may have to choose between complying with the long-term commitments specified in Senate Bill 350 and continuing to operate because they cannot acquire resources at the specified market price benchmarks that value the entire utility portfolio according to the CPUC.

CCAs may have to choose between complying with the long-term commitments specified in Senate Bill 350 and continuing to operate because they cannot acquire resources at the specified market price benchmarks that value the entire utility portfolio according to the CPUC.

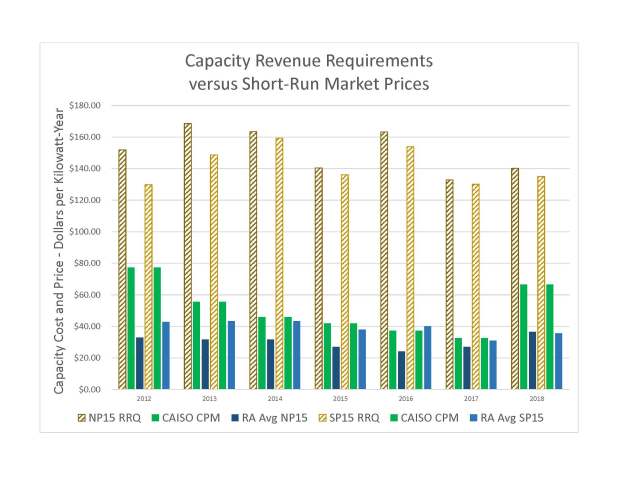

The chart above compares the revenue shortfalls that need to be made up from other capacity sales products to finance resource additions. The CAISO has reported for every year since 2001 that its short-run market clearing prices that were adopted as the market price benchmark in the PCIA have been insufficient to support new conventional generation investment. The chart above shows the results of the CAISO Annual Report on Market Issues and Performance compiled from 2012 to 2018, separated by north (NP15 RRQ) and south (SP15 RRQ) revenue requirements for new resources. (The historic data shows that CAISO revenues have never been sufficient to finance a resource addition.) The CAISO signs capacity procurement (CPM) agreements to meet near-term reliability shortfalls which is one revenue source for a limited number of generators. The other short run price is the resource adequacy credits transacted by load serving entities (LSE) such as the utilities and CCAs. This revenue source is available to a broader set of resources. However, neither of revenues come close to closing the cost shortfall for new capacity.

The CPUC and the CAISO have deliberately suppressed these market prices to avoid the price spikes and reliability problems that occurred during the 2000-2001 energy crisis. By explicit state policy, these market prices are not to be used for assessing resource acquisition benchmarks. Yet, the CPUC adopted in its PCIA OIR decision (D.18-10-019) exactly this stance by asserting that the CCAs must be able to acquire new resources at less than these prices to beat the benchmarks used to calculate the PCIA. The CPUC used the CAISO energy prices plus the average RA prices as the base for the market value benchmark that represents the CCA threshold.

In a functioning market, the relevant market prices should indicate the relative supply-demand balance–if supply is short then prices should rise sufficiently to cover the cost of new entrants. Based on the relative price balance in the chart, no new capacity resources should be needed for some time.

Yet the CPUC recently issued a decision (D.19-04-040) that ordered procurement of 2,000 MW of capacity for resource adequacy. And now the CPUC proposes to up that target to 4,000 MW by 2021. All of this runs counter to the price signals that CPUC claims represent the “market value” of the assets held by the utilities.

If the CCAs purchase resources that cost more than the PCIA benchmarks then they will be losing money for their ratepayers (note that CCAs have no shareholders). Most often long-term power purchase agreements (PPA) have prices above the short-term prices because those short-term prices do not cover all of the values transacted in the market place. (More on that in the near future.) The CPUC should either align its market value benchmarks with its resource acquisition directives or acknowledge that their directives are incorrect.