The freeze and resulting rolling outages in Texas in February highlighted the unique structure of the power market there. Customers and businesses were left with huge bills that have little to do with actual generation expenses. This is a consequence of the attempt by Texas to fit into an arcane interpretation of an economic principle where generators should be able to recover their investments from sales in just a few hours of the year. Problem is that basic of accounting for those cashflows does not match the true value of the power in those hours.

The Electric Reliability Council of Texas (ERCOT) runs an unusual wholesale electricity market that supposedly relies solely on hourly energy prices to provide the incentives for incenting new generation investment. However, ERCOT is using the same type of administratively-set subsidies to create enough potential revenue to cover investment costs. Further, a closer examination reveals that this price adder is set too high relative to actual consumer value for peak load power. All of this leads to a conclusion relying solely on short-run hourly prices as a proxy for the market value that accrues to new entrants is a misplaced metric.

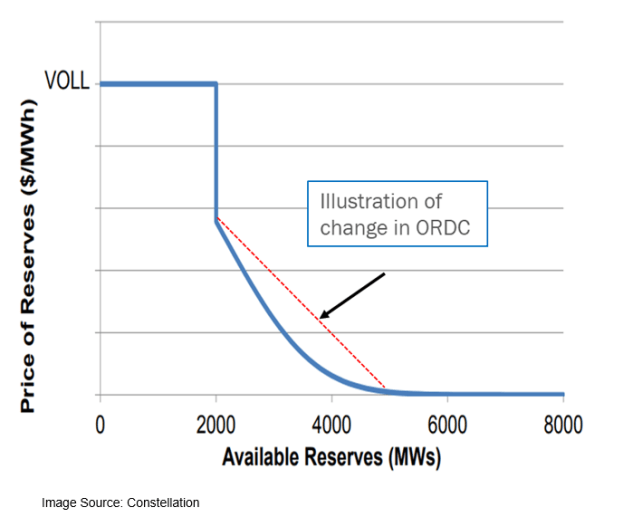

The total ERCOT market first relies on side payments to cover commitment costs (which creates barriers to entry but that’s a separate issue) and second, it transfers consumer value through to the Operating Reserve Demand Curve (ORDC) that uses a fixed value of lost load (VOLL) in an arbitrary manner to create “opportunity costs” (more on that definition at a later time) so the market can have sufficient scarcity rents. This second price adder is at the core of ERCOT’s incentive system–energy prices alone are insufficient to support new generation investment. Yet ERCOT has ignored basic economics and set this value too high based on both available alternatives to consumers and basic regional budget constraints.

I started with an estimate of the number of hours where prices need the ORDC to be at full VOLL of $9000/MWH to recover the annual revenue requirements of combustion turbine (CT) investment based on the parameters we collected for the California Energy Commission. It turns out to be about 20 to 30 hours per year. Even if the cost in Texas is 30% less, this is still more 15 hours annually, every single year or on average. (That has not been happening in Texas to date.) Note for other independent system operators (ISO) such as the California ISO (CAISO), the price cap is $1,000 to $2,000/MWH.

I then calculated the cost of a customer instead using a home generator to meet load during those hours assuming a life of 10 to 20 years on the generator. That cost should set a cap on the VOLL to residential customers as the opportunity cost for them. The average unit is about $200/kW and an expensive one is about $500/kW. That cost ranges from $3 to $5 per kWh or $3,000 to $5,000/MWH. (If storage becomes more prevalent, this cost will drop significantly.) And that’s for customers who care about periodic outages–most just ride out a distribution system outage of a few hours with no backup. (Of course if I experienced 20 hours a year of outage, I would get a generator too.) This calculation ignores the added value of using the generator for other distribution system outages created by events like a hurricane hitting every few years, as happens in Texas. That drives down this cost even further, making the $9,000/MWH ORDC adder appear even more distorted.

The second calculation I did was to look at the cost of an extended outage. I used the outages during Hurricane Harvey in 2017 as a useful benchmark event. Based on ERCOT and U.S. Energy Information Reports reports, it looks like 1.67 million customers were without power for 4.5 days. Using the Texas gross state product (GSP) of $1.9 trillion as reported by the St. Louis Federal Reserve Bank, I calculated the economic value lost over 4.5 days, assuming a 100% loss, at $1.5 billion. If we assume that the electricity outage is 100% responsible for that loss, the lost economic value per MWH is just under $5,000/MWH. This represents the budget constraint on willingness to pay to avoid an outage. In other words, the Texas economy can’t afford to pay $9,000/MWH.

The recent set of rolling blackouts in Texas provides another opportunity to update this budget constraint calculation in a different circumstance. This can be done by determining the reduction in electricity sales and the decrease in state gross product in the period.

Using two independent methods, I come up with an upper bound of $5,000/MWH, and likely much less. One commentator pointed out that ERCOT would not be able achieve a sufficient planning reserve level at this price, but that statement is based on the premises that short-run hourly prices reflect full market values and will deliver the “optimal” resource mix. Neither is true.

This type of hourly pricing overemphasizes peak load reliability value and undervalues other attributes such as sustainability and resilience. These prices do not reflect the full incremental cost of adding new resources that deliver additional benefits during non-peak periods such as green energy, nor the true opportunity cost that is exercised when a generator is interconnected rather than during later operations. Texas has overbuilt its fossil-fueled generation thanks to this paradigm. It needs an external market based on long-run incremental costs to achieve the necessary environmental goals.