The Energy Institute’s blog has an important premise–that solar rooftop customers have imposed costs on other ratepayers with few benefits. This premise runs counter to the empirical evidence.

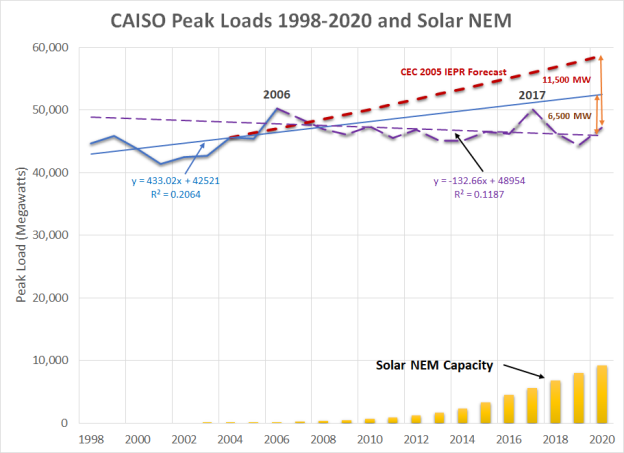

First, these customers have deferred an enormous amount of utility-scale generation. In 2005 the CEC forecasted the 2020 CAISO peak load would 58,662 MW. The highest peak after 2006 has been 50,116 MW (in 2017–3,000 MW higher than in August 2020). That’s a savings of 8,546 MW. (Note that residential installations are two-thirds of the distributed solar installations.) The correlation of added distributed solar capacity with that peak reduction is 0.938. Even in 2020, the incremental solar DER was 72% of the peak reduction trend. We can calculate the avoided peak capacity investment from 2006 to today using the CEC’s 2011 Cost of Generation model inputs. Combustion turbines cost $1,366/kW (based on a survey of the 20 installed plants–I managed that survey) and the annual fixed charge rate was 15.3% for a cost of $209/kW-year. The total annual savings is $1.8 billion. The total revenue requirements for the three IOUs plus implied generation costs for DA and CCA LSEs in 2021 was $37 billion. So the annual savings that have accrued to ALL customers is 4.9%. Given that NEM customers are about 4% of the customer base, if those customers paid nothing, everyone else’s bill would only go up by 4% or less than what rooftop solar has saved so far.

In addition, the California Independent System Operator (CAISO) calculated in 2018 that at least $2.6 billion in transmission projects had been deferred through installed distributed solar. Using the amount installed in 2017 of 6,785 MW, the avoided costs are $383/kW or $59/kW-year. This translates to an additional $400 million per year or about 1.1% of utility revenues.

The total savings to customers is over $2.2 billion or about 6% of revenue requirements.

Second, rooftop solar isn’t the most expensive power source. My rooftop system installed in 2017 costs 12.6 cents/kWh (financed separately from our mortgage). In comparison, PG&E’s RPS portfolio cost over 12 cents/kWh in 2019 according to the CPUC’s 2020 Padilla Report, plus there’s an increments transmission cost approaching 4 cents/kWh, so we’re looking at a total delivered cost of 16 cents/kwh for existing renewables. (Note that the system costs to integrate solar are largely the same whether they are utility scale or distributed).

Comparing to the average IOU RPS portfolio cost to that of rooftop solar is appropriate from the perspective of a customer. Utility customers see average, not marginal, costs and average cost pricing is widely prevalent in our economy. To achieve 100% renewable power a reasonable customer will look at average utility costs for the same type of power. We use the same principle by posting on energy efficient appliances the expect bill savings based on utility rates–-not on the marginal resource acquisition costs for the utilities.

And customers who would choose to respond to the marginal cost of new utility power instead will never really see those economic savings because the supposed savings created by that decision will be diffused across all customers. In other words, other customers will extract all of the positive rents created by that choice. We could allow for bypass pricing (which industrial customers get if they threaten to leave the service area) but currently we force other customers to bear the costs of this type of pricing, not shareholders as would occur in other industries. Individual customers are currently the decision making point of view for most energy use purposes and they base those on average cost pricing, so why should we have a single carve out for a special case that is quite similar to energy efficiency?

I wrote more about whether a fixed connection cost is appropriate for NEM customers and the complexity of calculating that charge earlier this week.