My previous post, Part 1, showed how California’s utilities’ share prices have risen well above the average across utilities despite claims that investors are risk averse to the California utilities. That valuation premium reflects an excessively high authorized return on equity (ROE) from the California Public Utilities Commission (CPUC).

The utilities’ market values can then be linked to the utilities’ book values and authorized returns on equity to calculate the implied market returns on equity. The authorized income per share is the authorized ROE multiplied by the book value per share. That income is divided by the market share price to arrive at the implied market return on equity for that company. Both Sempra (SRE) and Edison International (EIX) significantly outperform the Dow Jones Utility average and PG&E Corporation (PGC) maintained the same trend until market had significant concerns about the company’s role in the 2017 wildfires.

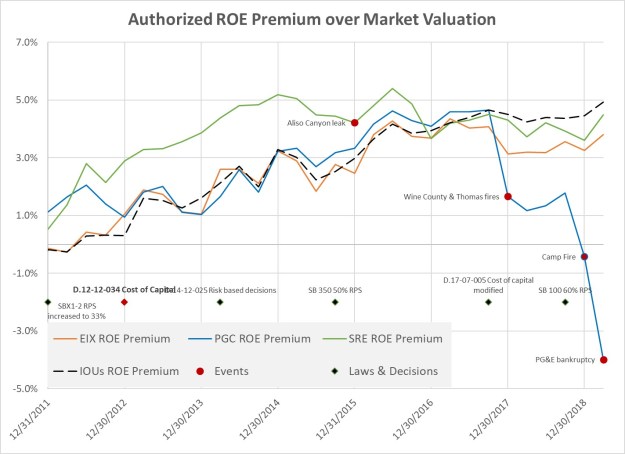

The figure above tracks the difference or premium value of the authorized ROE over the market valuation of that ROE. A premium value of zero means that the market valuation is on par with the authorized ROE. A higher or positive premium value means that investors see the utility’s equity shares as attractive investments with lower risks than the assessments of the commissions that set the authorized ROEs. In other words, a commission is providing an overly generous incentive to investors if the premium value is positive. The figure above compares the market implied ROE for the three California holding companies to a market basket of 10 U.S. holding companies that own 17 electric and gas utilities, and do not own significant non-utility subsidiaries.

At the time of the 2012 cost of capital decision, the authorized ROEs for the California utilities and the basket of U.S. utilities were close to the implied market ROEs. Except for Sempra, which was an outlier as evidenced by its share price growth relative to the other utilities, the authorized ROE was within 100 basis points of the implied market ROE at the end of 2012. For both Edison International and PG&E Corporation, the authorized ROE and the implied market ROE on December 31, 2012 were exactly on par—10.5% for Edison and 10.4% for PG&E. Only Sempra showed a positive premium of 300 basis points as a result of a rapid increase in market value over 2012.

Over the period from 2012 to late 2017, the implied market ROEprogressed steadily downward–that is, the market value premium increased–for both the California utilities and the other U.S. utilities. Sempra’s premium leveled off in late 2014 and has drifted downward since without any significant corrections. SCE’s diverged upward some from the U.S. utilities mid-2016, but again there are not sharp changes in direction, even with the Thomas Fire in late 2017. PG&E followed the same pattern as SCE until the Wine Country fires in late 2017, and took another sharp turn with the Camp Fire and, understandably, the subsequent voluntary bankruptcy filing.

We can see at the end of September 2017, just after the last Commission decision on cost of capital, the market premium for the 10 utilities had grown to 470 basis points. The premiums for PG&E, Edison and Sempra all lied in a narrow band between 410 basis points for Edison and 470 basis points for PG&E. In other words, 1) California utility investors were receiving overly generous returns on their investments as evidenced in the share prices, and 2) California utility investors have not been demanding a significant discount for perceived increased risk compared to other U.S. utilities, contrary to the assertions by the utilities’ witnesses in this proceeding.

More on the national scene from John Farrell: https://www.linkedin.com/pulse/how-utility-profits-drive-energy-affordability-crisis-john-farrell-xx0dc/

LikeLike

Pingback: Utilities’ returns are too high (Part 1) | Economics Outside the Cube

The LA Times interviewed EDF’s Michael Colvin about its role in pushing for lower returns and using this policy to begin the phase out of natural gas. https://www.latimes.com/environment/story/2019-12-02/higher-profits-pge-southern-california-edison-regulators-arent-convinced

LikeLike