Meredith Fowlie wrote this blog on the proposal to drastically increase California utilities’ residential fixed charges at the Energy Institute at Haas blog. I posted this comment (with some additions and edits) in response.

First, infrastructure costs are responsive to changes in both demand and added generation. It’s just that those costs won’t change for a customer tomorrow–it will take a decade. Given how fast transmission retail rates have risen and have none of the added fixed costs listed here, the marginal cost must be substantially above the current average retail rates of 4 to 8 cents/kWh.

Further, if a customer is being charged a fixed cost for capacity that is being shared with other customers, e.g., distribution and transmission wires, they should be able to sell that capacity to other customers on a periodic basis. While many economists love auctions, the mechanism with the lowest ancillary transaction costs is a dealer market akin a grocery store which buys stocks of goods and then resells. (The New York Stock Exchange is a type of dealer market.) The most likely unit of sale would be in cents per kWh which is the same as today. In this case, the utility would be the dealer, just as today. So we are already in the same situation.

Airlines are another equally capital intensive industry. Yet no one pays a significant fixed charge (there are some membership clubs) and then just a small incremental charge for fuel and cocktails. Fares are based on a representative long run marginal cost of acquiring and maintaining the fleet. Airlines maintain a network just as utilities. Economies of scale matter in building an airline. The only difference is that utilities are able to monopolistically capture their customers and then appeal to state-sponsored regulators to impose prices.

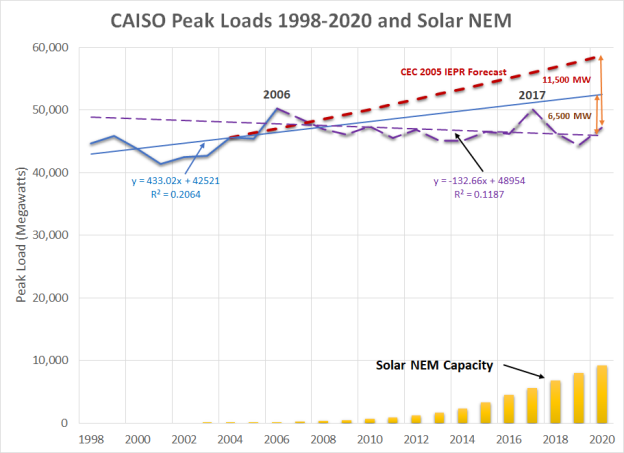

Why are California’s utility rates 30 to 50% or more above the current direct costs of serving customers? The IOUs, and PG&E in particular, over procured renewables in the 2010-2012 period at exorbitant prices (averaging $120/MWH) in part in an attempt to block entry of CCAs. That squandered the opportunity to gain the economics benefits from learning by doing that led to the rapid decline in solar and wind prices over the next decade. In addition, PG&E refused to sell a part of its renewable PPAs to the new CCAs as they started up in the 2014-2017 period. On top of that, PG&E ratepayers paid an additional 50% on an already expensive Diablo Canyon due to the terms of the 1996 Settlement Agreement. (I made the calculations during that case for a client.) And on the T&D side, I pointed out beginning in 2010 that the utilities were overforecasting load growth and their recorded data showed stagnant loads. The peak load from 2006 was the record until 2022 and energy loads have remained largely constant, even declining over the period. The utilities finally started listening the last couple of years but all of that unneeded capital is baked into rates. All of these factors point not to the state or even the CPUC (except as an inept monitor) as being at fault, but rather to the utilities’ mismanagement.

Using Southern California Edison’s (SCE) own numbers, we can illustrate the point. SCE’s total bundled marginal costs in its rate filing are 10.50 cents per kWh for the system and 13.64 cents per kWh for residential customers. In comparison, SCE’s average system rate is 17.62 cents per kWh or 68% higher than the bundled marginal cost, and the average residential rate of 22.44 cents per kWh is 65% higher. From SCE’s workpapers, these cost increases come primarily from four sources.

- First, about 10% goes towards various public purpose programs that fund a variety of state-initiated policies such as energy efficiency and research. Much of this should be largely funded out of the state’s General Fund as income distribution through the CARE rate instead. And remember that low income customers are already receiving a 35% discount on rates.

- Next, another 10% comes roughly from costs created two decades ago in the wake of the restructuring debacle. The state has now decreed that this revenue stream will instead be used to pay for the damages that utilities have caused with wildfires. Importantly, note that wildfire costs of any kind have not actually reached rates yet. In addition, there are several solutions much less costly than the undergrounding proposed by PG&E and SDG&E, including remote rural microgrids.

- Approximately 15% is from higher distribution costs, some of which have been created by over-forecasting load growth over the last 15 years; loads have remained stagnant since 2006.

- And finally, around 33% is excessive generation costs caused by paying too much for purchased power agreements signed a decade ago.

An issue raised as rooftop solar spreads farther is the claim that rooftop solar customers are not paying their fair share and instead are imposing costs on other customers, who on average have lower incomes than those with rooftop solar. Yet the math behind the true rate burden for other customers is quite straightforward—if 10% of the customers are paying essentially zero (which they are actually not), the costs for the remaining 90% of the customers cannot go up more than 11% [100%/(100%-10%) = 11% ]. If low-income customers pay only 70% of this—the 11%– then their bills might go up about 8%–hardly a “substantial burden.” (70% x 11% = 7.7%)

As for aligning incentives for electrification, we proposed a more direct alternative on behalf of the Local Government Sustainable Energy Coalition where those who replace a gas appliance or furnace with an electric receive an allowance (much like the all-electric baseline) priced at marginal cost while the remainder is priced at the higher fully-loaded rate. That would reduce the incentive to exit the grid when electrifying while still rewarding those who made past energy efficiency and load reduction investments.

The solution to high rates cannot come from simple rate design; as Old Surfer Dude points out, wealthy customers are just going to exit the grid and self provide. Rate design is just rearranging the deck chairs. The CPUC tried the same thing in the late 1990s with telcom on the assumption that customers would stay put. Instead customers migrated to cell phones and dropped their land lines. The real solution is going to require some good old fashion capitalism with shareholders and associated stakeholders absorbing the costs of their mistakes and greed.

NBC Bay Area: ‘This is nuts’: PG&E customers stunned by first bills since rate hikes.

https://www.nbcbayarea.com/news/local/pge-rate-hikes-customers-bills/3433825/

LikeLike