From Utility Dive: The Salem NGS Unit 2 in New Jersey shutdown due to ice forming in its cooling water intake during the latest polar vortex event.

From Utility Dive: The Salem NGS Unit 2 in New Jersey shutdown due to ice forming in its cooling water intake during the latest polar vortex event.

Texas generated 30% of its electricity last year with carbon-free resources (mostly wind.) Coals has shrunk over the last decade from 37% to 25%.

PG&E spends $275 million a year on energy efficiency investments that reduce demand by 100 MW. It also spends $65 million a year on demand response to reduce peak loads by 400 MW. If we assume that energy efficiency investments are effective an average of 12 years the incremental cost of those investments is $66 per MWH (6.6 cents per kWh). For demand response the incremental cost, which should match the market value, is $163 per kilowatt-year (or $13.60 per kW-month). Both of these values are reasonable investments for long-term resources.

Yet, PG&E argues in the PCIA exit fee proceeding and its annual ERRA generation cost proceeding that the appropriate market valuation for its resources are the short-term fire sale values that it realizes in the daily markets. According to PG&E, customers do not realize any additional value from holding these resources beyond what those resources can be bought and sold for the CAISO markets and in bilateral short-term deals.

So we are left with the obvious question: Why is PG&E continuing to invest in energy efficiency and demand response if the utility states that it can meet all of its needs in the short-term markets? This hypocrisy is probably best explained by PG&E manipulating the regulatory process. PG&E’s proposed “market valuation” sets the exit fee for community choice aggregation (CCA) at a high level. Instead, that market valuation should reflect how much CCAs have saved bundled customers in avoided procurement, and what PG&E pays for adding new resources.

Kevin Novan from UC Davis wrote an article in the University of California Giannini Foundation’s Agriculture and Resource Economics Update entitled “Should Communities Get into the Power Marketing Business?” Novan was skeptical of the gains from community choice aggregation (CCA), concluding that continued centrally planned procurement was preferable. Other UC-affiliated energy economists have also expressed skepticism, including Catherine Wolfram, Severin Borenstein, and Maximilian Auffhammer.

At the heart of this issue is the question of whether the gains of “perfect” coordination outweigh the losses from rent-seeking and increased risks from centralized decision making. I don’t consider myself an Austrian economist, but I’m becoming a fan of the principle that the overall outcomes of many decentralized decisions is likely to be better than a single “all eggs in one basket” decision. We pretend that the “central” planner is somehow omniscient and prudently minimizes risks. But after three decades of regulatory practice, I see that the regulators are not particularly competent at choosing the best course of action and have difficulty understanding key concepts in risk mitigation.By distributing decision making, we better capture a range of risk tolerances and bring more information to the market place. There are further social gains from dispersed political decision making that brings accountability much closer to home and increases transparency. Of course, there’s a limit on how far decentralization should go–each household can’t effectively negotiate separate power contracts. But we gain much more information by adding a number of generation service providers or “load serving entities” (LSE) to the market.

I found several shortcomings with with Novan’s article that would change the tenor. I take each in turn:

I was on the City of Davis Community Choice Energy Advisory Committee, and I am testifying on behalf of the California CCAs on the setting of the PCIA in several dockets. I have a Ph.D. from Berkeley’s ARE program and have worked on energy, environmental and water issues for about 30 years.

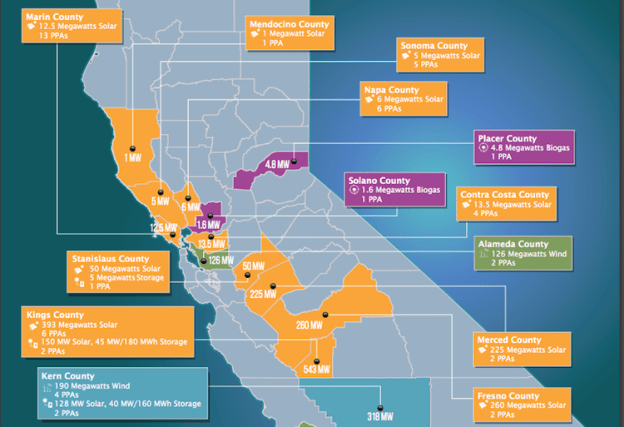

California’s community choice aggegrators (CCAs) are on track to meet their state-mandated renewable portfolio standard obligations. PG&E, SCE and SDG&E have not signed significant new renewable power capacity since 2015, while CCAs have been building new projects. To achieve zero carbon electricity by 2050 will require aggressive plans to procure new renewables soon.

——

Rather than focus on CCA procurement, the CPUC would better serve the state to use the provisions of AB 57 (e.g., PUC Section 454.5(b)(6)) and its other authorities, including those still in force from AB 1890 (1996). PG&E and SCE already collected $7 billion on an accelerated basis during the “competitive transition period” from 1998 to 2001 towards their legacy utility-owned generation resources such as Diablo Canyon, San Onofre and their hydropower generation. SDG&E completely paid off its generation portfolio in 1999 this way. Further, PG&E had already recovered its entire investment in Diablo Canyon by December 31, 1997 prior to the start of the opening of the restructured market. (I tracked the CTC accounts throughout the period, reporting to the CEC in 2001, and calculated the return on investment in Diablo Canyon for settlement discussions in 1996.) If the Commission wanted to repay the debts incurred during the 2000-01 energy crisis, the better solution, which it did in part with SCE, would have been to simply establish a “regulatory asset” with no connection to the generating facilities which had already been paid off. As it is, customers-–bundled and departed–are paying twice (and THREE times in the case of Diablo Canyon) for the same power plants.

The IOUs currently lack any real incentives to control their portfolio costs, as evidenced by their bundled portfolio plans for PG&E and SCE. Those plans say nothing about minimizing costs or managing risks except to avoid incurring shareholder penalties for missing the RPS mandates. In fact, PG&E has accrued a 3.3 cents per kilowatt-hour premium above the market value of its RPS portfolio to protect against a potential “price spike” between now and 2027. It is no wonder that customers have become unhappy with how the IOUs have managed their generation portfolios.

As I listen to the opening of the joint California Customer Choice En Banc held by the CPUC and CEC, I hear Commissioners and speakers claiming that community choice aggregators (CCAs) are taking advantage of the current market and shirking their responsibilities for developing a responsible, resilient resource portfolio.

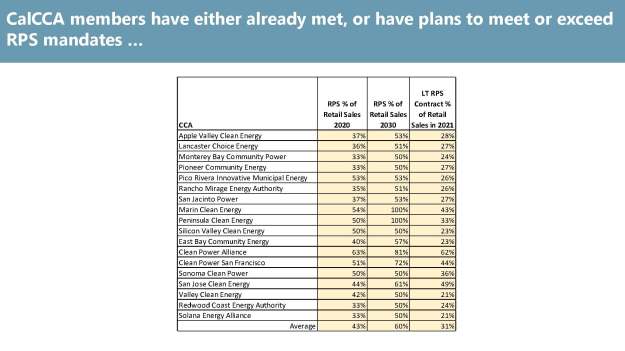

The CPUC’s view has two problems. The first is an unreasonable expectation that CCAs can start immediately as a full-grown organization with a complete procurement organization, and more importantly, a rock solid credit history. The second is how the CPUC has ignored the fact that the CCAs have already surpassed the state’s RPS targets in most cases and that they have significant shares of long-term power purchase agreements (PPAs).

State law in fact penalizes excess procurement of RPS-eligible power by requiring that 65% of that specific portfolio be locked into long-term PPAs, regardless of the prudency of that policy. PG&E has already demonstrated that they have been unable to prudently manage its long-term portfolio, incurring a 3.3 cents per kilowatt-hour risk hedge premium on its RPS portfolio. (Admittedly, that provision could be interpreted to be 65% of the RPS target, e.g., 21.5% of a portfolio that has met the 33% RPS target, but that is not clear from the statute.)

In its annual report on resource adequacy (RA) transactions, the CPUC reports the wrong result for the market price to be used for valuing capacity from the RA market data. The Commission’s decision issued in the PCIA rulemaking on establishing the CCA’s “exit fee” uses this value in error. In the CAISO energy and ancillary services markets, the market clearing price used to set the value of the energy portfolio is determined by the highest accepted bid in a single hour, and then averaged across all hours. In contrast, the average reported RA price in The 2017 Resource Adequacy Report incorrectly reports the average of all transactions. This would be equivalent to the CAISO reporting the average of all accepted bids, including those at zero or even negative, as the market clearing price.

The appropriate RA price metric is the highest RA transaction price for each month. This price represents the market equilibrium point at which a consumer is willing to pay the highest price given how low a price a supplier is willing to provide that quantity of the resource. (The other transactions are called “inframarginal” and such transactions are common in many markets.) In a full auction market, all transactions would clear at this single price, which is why the CAISO reports a single market clearing price for all transactions in a single hour. That should also be the case for the RA market price, except the time unit is a month.

Due to a lack of an auction for the moment, it is possible to manipulate the highest apparent price through a bilateral transaction. Instead, the Commission could choose a price near the highest point, but with sufficient market depth to mitigate potential manipulation. Using the 90th percentile transaction is one metric commonly used based on a quick survey of market price reports.

Nick Chaset is the CEO of East Bay Community Energy which is a community choice aggregator (CCA) that serves Alameda County. He also was Commission President Michael Picker’s chief advisor until last year when he left for EBCE. He explains in this article how two proposed decisions that the CPUC is considering are fundamentally wrong and will shift cost onto CCA customers. (I testified on behalf of CalCCA in this proceeding. I’ll have more on this before the Commission’s scheduled vote October 11.)

Figure 1 – CPUC’s Proposed Resource Adequacy Value vs. True Market Values

Figure 2 – GHG Premium Value Missing from CPUC Proposed Decision

Figure 3 – Falling Utility Rates as Customers Depart Filed in Their ERRA Rate Applications

I received a notice of a new MIT study entitled “The Future of Nuclear Energy in a Carbon-Constrained World” which looks at the technological, regulatory and economic changes required to make nuclear power viable again. A summary states

The findings are that new policy models and cost-cutting technologies would help nuclear play vital role in climate solutions. Progress in reducing carbon emissions requires a broad range of actions to effectively leverage nuclear energy.

However, nothing in the summary reveals the paradigm-shattering innovation that will be required to make nuclear power competitive with a diverse fleet of renewables plus storage that would achieve the same goals. The cost of a solar plant plus storage with today’s technology still costs less than a current technology nuclear plant. That alternative fleet would also provide better reliability by diversifying the generation sources through smaller plants and avoid any radiation contamination risk.

The nuclear industry must clearly demonstrate that it can get past the many hurdles that led to the recent cancellation of two projects in the southeast U.S. Reviving nuclear power will require more than fantasies about what might be.

All Things Solar and Electric

Musings from M.Cubed on the environment, energy and water

This blog is not necessarily about biking. It's about life that is lived locally, at a human pace.

Energy, Environment and Policy

Musings from M.Cubed on the environment, energy and water

Examining State Authority in Interstate Electricity Markets

Musings from M.Cubed on the environment, energy and water

Musings from M.Cubed on the environment, energy and water

Economic insight and analysis from The Wall Street Journal.

Musings from M.Cubed on the environment, energy and water

Musings from M.Cubed on the environment, energy and water

A few thoughts from John Fleck, a writer of journalism and other things, living in New Mexico

Musings from M.Cubed on the environment, energy and water

Musings from M.Cubed on the environment, energy and water

Musings from M.Cubed on the environment, energy and water

Tips and tricks on programming, evolutionary algorithms, and doing research

Musings from M.Cubed on the environment, energy and water

A blog about water resources and law

Musings from M.Cubed on the environment, energy and water