Yolo County and the City of Davis became the latest community to approve a CCE (for community choice energy, an alternative moniker to the legalistic community choice aggregation). I sat on the advisory committee assessing options and the business case is strong for the viability of this option. This is the leading edge of a wave of CCEs across California. The combination of market conditions, falling renewable power costs, recognition of changes in the electricity market, and dissatisfaction with the incumbent utilities is pushing broad community coalitions to take the leap.

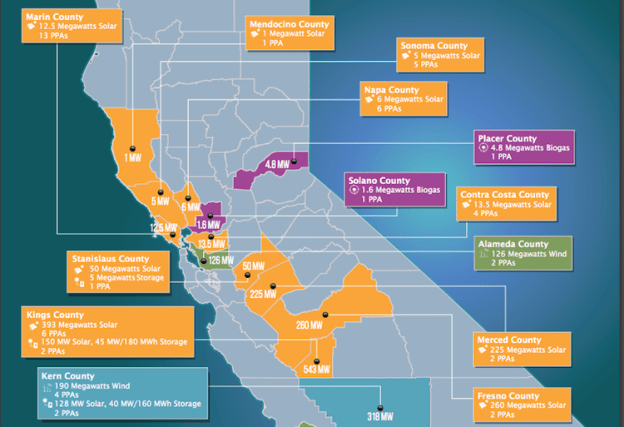

To date three communities have operating CCE’s, with MCE starting first in 2010. MCE is made up of not only Marin County, but also Napa County, and the City of Richmond and Benecia. It also is considering adding new members. It currently has 17 voting communities. Sonoma Clean Power followed in 2014, and is considering adding Lake and Mendocino counties. The City of Lancaster started in late 2015 in SCE’s service territory. Peninsula Clean Energy, composed of San Mateo County and its cities, kicked off service in 2016. In addition, San Francisco has approved a CCE but has had various political barriers to getting off the ground.

To date three communities have operating CCE’s, with MCE starting first in 2010. MCE is made up of not only Marin County, but also Napa County, and the City of Richmond and Benecia. It also is considering adding new members. It currently has 17 voting communities. Sonoma Clean Power followed in 2014, and is considering adding Lake and Mendocino counties. The City of Lancaster started in late 2015 in SCE’s service territory. Peninsula Clean Energy, composed of San Mateo County and its cities, kicked off service in 2016. In addition, San Francisco has approved a CCE but has had various political barriers to getting off the ground.

Here’s a couple websites that show maps and lists of what counties and cities are pursuing CCAs (the lists are slightly different).

Other communities in the midst of either approving or implementing new CCEs include:

Alameda County

Contra Costa County – considering joining Alameda or MCE, or going it alone

Humboldt County as Redwood Coast Energy Authority – considering joining SCP or going alone

South Bay Cities of Los Angeles County as South Bay Clean Power

Los Angeles County

Monterey, Santa Cruz and San Benito Counties and their cities as Monterey Bay Community Power

Riverside and San Bernardino Counties – issued RFP for joint study

San Diego County

City of San Diego – issued RFP for a study

City of Solana Beach

Santa Clara County and 11 cities as Silicon Valley CCE Partners – starting late 2016

City of San Jose – exploring joining SVCCEP or going alone

Santa Barbara County, San Luis Obispo County and Ventura County – released study on feasibility and options

City of Walnut Creek – considering joining with Contra Costa or going alone

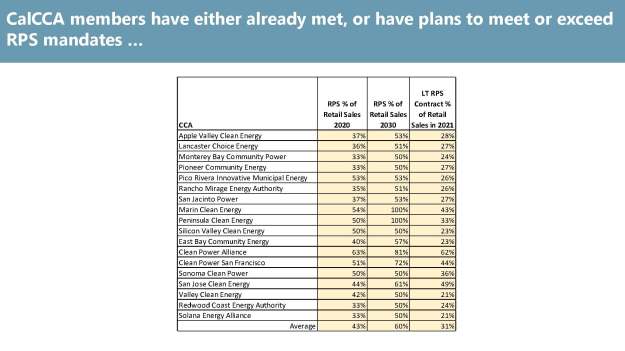

All of this activity has serious implications for IOU purchasing and contract management going forward, CPUC regulation and overall procurement transparency. The IOUs and CPUC have operated in black box to date claiming that confidentiality is necessary to prevent market manipulation. Yet with all of these CCEs likely operating as open books, everyone will have the market information that the IOUs claim is so vital to protect. This is likely to open up IOU PPAs to greater scrutinty–attention that neither the IOUs or the CPUC probably want.