I read these two statements in his blog post and come to a very different conclusions:

“(I)ndividuals and businesses make investments in response to those policies, and many come to believe that they have a right to see those policies continue indefinitely.”

Why wasn’t there a similar cry against bailing out PG&E in not one but TWO bankruptcies? Both PG&E and SCE have clearly relied on the belief that they deserve subsidies to continue staying in business. (SCE has ridden along behind PG&E in both cases to gain the spoils.) The focus needs to be on ALL players here if these types of subsidies are to be called out.

“(T)he reactions have largely been about how much subsidy rooftop solar companies in California need in order to stay in business.”

We are monitoring two very different sets of media then. I see much more about the ability of consumers to maintain an ability to gain a modicum of energy independence from large monopolies that compel that those consumers buy their service with no viable escape. I also see a reactions about how this will undermine directly our ability to reduce GHG emissions. This directly conflicts with the CEC’s Title 24 building standards that use rooftop solar to achieve net zero energy and electrification in new homes.

Yes, there are problems with the current compensation model for NEM customers, but we also need to recognize our commitments to customers who made investments believing they were doing the right thing. We need to acknowledge the savings that they created for all of us and the push they gave to lower technology costs. We need to recognize the full set of values that these customers provide and how the current electric market structure is too broken to properly compensate what we want customers to do next–to add more storage. Yet, the real first step is to start at the source of the problem–out of control utility costs that ratepayers are forced to bear entirely.

Last month the California Public Utilities Commission (CPUC) issued a decision in Phase II of the PG&E 2020 General Rate Case that endorsed all but one of my proposals on behalf of the Agricultural Energy Consumers Association (AECA) to better align revenue allocation with a rational approach to using marginal costs. Most importantly the CPUC agreed with my observation that the energy system is changing too rapidly to adopt a permanent set of rate setting principles as PG&E had advocated for. For now, we will continue to explore options as relationships among customers, utilities and other providers evolve.

At the heart of the matter is the economic principle that prices are set most efficiently when they adhere to the marginal cost or the cost of producing the last unit of a good or service. In a “standard” market, marginal costs are usually higher than the average cost so a producing firm generates a profit with each sale. For utilities, this is often not true–the average costs are higher than the marginal costs, so we need a means of allocating those additional costs to ensure that the utilities continue to be viable entities. California uses a “second-best” economic method called “Ramsey pricing” that applies relative marginal costs to serve different customers to allocate revenue responsibility.

I made four key proposals on how to apply marginal cost principles for rate setting purposes:

Proposes an updated agricultural load forecasting method that is more accurate and incorporates only public data and currently known variables that can predict next year’s load more accurately.

Use PCIA exit fee market price benchmarks (MPBs) to give consistent revenue allocation across rate classes and bundled vs departed customers.

Include renewable energy credits (REC) in the marginal energy costs (MEC) to reflect incremental RPS acquisition and consistency with the PCIA MPB.

Use the resource adequacy (RA) MPB for setting the marginal generation capacity cost (MGCC) due to uncertainty about resource type for capacity and for consistency with the PCIA MPB.

Marginal customer access costs (MCAC) should be calculated by using the depreciated replacement cost for existing services (RCNLD), and new services costs added for the new customers added as growth.

PG&E settled with AECA on the first to change its agricultural load forecasting methodology in upcoming proceedings. The CPUC agreed with AECA’s positions on two of the other three (RECs in the MEC, and MCAC). And on the third related to MGCC, the adopted position differed little materially.

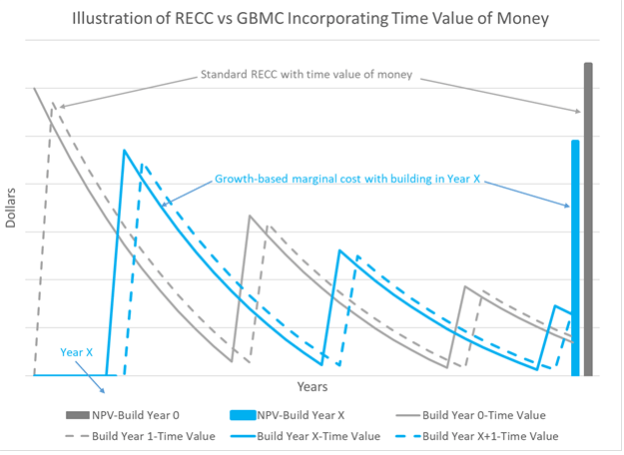

The most surprising was the choice to use the RCNLD costs for existing customer connections. The debate over how to calculate the MCAC has raged for three decades. Industrial customers preferred valuing all connections, new and existing, at the cost of new connection using the “real economic carrying cost” (RECC) method. This is most consistent with a simple reading of marginal cost pricing principles. On the other side, residential customer advocates claimed that existing connections were sunk costs and have a value of zero for determining marginal, inventing the “new customer only” (NCO) method. I explained in my testimony that the RECC method fails to account for the reduced value of aging connections, but that those connections have value in the market place through house prices, just as a swimming pool or a bathroom remodel adds value. The diminished value of those connections can be approximated using the depreciation schedules that PG&E applies to determine its capital-related revenue requirements. The CPUC has used the RCNLD method to set the value for the sale of PG&E assets to municipal utilities.

The CPUC agreed with this approach which essentially is a compromise between the RECC and NCO method. The RCNLD acknowledges the fundamental points of both methods–that existing customer connections represent an opportunity value for customers but those connections do not have the same value as new ones.

The saying goes “No good deed goes unpunished.” The California Public Utilities Commission seems to have taken that motto to heart recently, and stands ready to penalize yet another group of customers who answered the clarion call to help solve the state’s problems by radically altering the rules for solar rooftops. Here’s three case studies of recent CPUC actions that undermine incentives for customers to act in the future in response to state initiatives: (1) farmers who invested in response to price incentives, (2) communities that pursued renewables more assertively, and (3) customers who installed solar panels.

Agriculture: Farmers have responded to past time of use (TOU) rate incentives more consistently and enthusiastically than any other customer class. Instead of being rewarded for their consistency, their peak price periods shifted from the afternoon to the early evening. Growers face much more difficulty in avoiding pumping during that latter period.

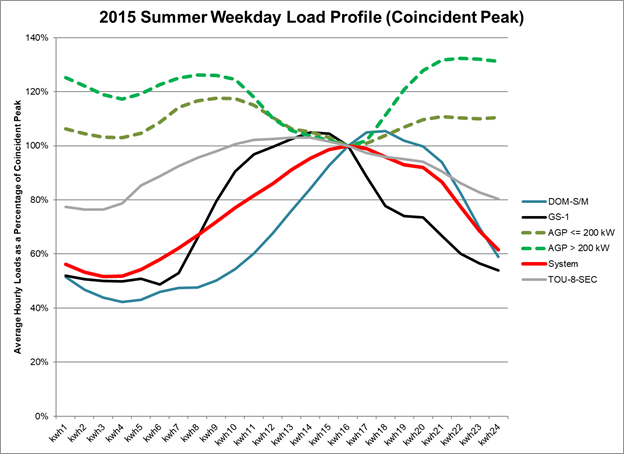

Since TOU rates were introduced to agricultural customers in the late 1970s, growers have made significant operational changes in response to TOU differentials between peak and off-peak energy prices to minimize their on-peak consumption. These include significant investments in irrigation equipment, storage and conveyance infrastructure and labor deployment rescheduling. The results of these expenditures are illustrated in the figure below, which shows how agricultural loads compare with system-wide load on a peak summer weekday in 2015, contrasting hourly loads to the load at the coincident peak hour. Both the smaller and larger agricultural accounts perform better than a range of representative rate schedules. Most notably agriculture’s aggregate load shape on a summer weekday is inverted relative to system peak, i.e., the highest agricultural loads occur during the lowest system load periods, in contrast with other rate classes.

All other rate schedules shown in the graphic hit their annual peak on the same peak day within the then-applicable peak hours of noon to 6 p.m. In contrast, agriculture electricity demand is less than 80% of its annual peak during those high-load hours, with its daily peak falling outside the peak period. Agriculture’s avoidance of peak hours occurred during the summer agricultural growing season, which coincided with peak system demand—just as the Commission asked customers to do. The Commission could not ask for a better aggregate response to system needs; in contrast to the profiles for all of the other customer groups, agriculture has significantly contributed to shifting the peak to a lower cost evening period.

The significant changes in the peak period price timing and differential that the CPUC adopted increases uncertainty over whether large investments in high water-use efficiency microdrip systems – which typically cost $2,000 per acre–will be financially viable. Microdrip systems have been adopted widely by growers over the last several years—one recent study of tomato irrigation rates in Fresno County could not find any significant quantity of other types of irrigation systems. Such systems can be subject to blockages and leaks that are only detectable at start up in daylight. Growers were able to start overnight irrigation at 6 p.m. under the legacy TOU periods and avoid peak energy use. In addition, workers are able to end their day shortly after 6 p.m. and avoid nighttime accidents. Shifting that load out of the peak period will be much more difficult to do with the peak period ending after sunset.

Contrary to strong Commission direction to incent customers to avoid peak power usage, the shift in TOU periods has served to penalize, and reverse, the great strides the agricultural class has made benefiting the utility system over the last four decades.

Community choice aggregators: CCAs were created, among other reasons, to develop more renewable or “green” power. The state achieved its 2020 target of 33% in large part because of the efforts of CCAs fostered through offerings of 50% and 100% green power to retail customers. CCAs also have offered a range of innovative programs that go beyond the offerings of PG&E, SCE and SDG&E.

Nevertheless, the difficulty of reaching clean energy goals is created by the current structure of the PCIA. The PCIA varies inversely with the market prices in the market–as market prices rise, the PCIA charged to CCAs and direct access (DA) customers decreases. For these customers, their overall retail rate is largely hedged against variation and risk through this inverse relationship.

The portfolios of the incumbent utilities are dominated by long-term contracts with renewables and capital-intensive utility-owned generation. For example, PG&E is paying a risk premium of nearly 2 cents per kilowatt-hour for its investment in these resources. These portfolios are largely impervious to market price swings now, but at a significant cost. The PCIA passes along this hedge through the PCIA to CCAs and DA customers which discourages those latter customers from making their own long term investments. (I wrote earlier about how this mechanism discouraged investment in new capacity for reliability purposes to provide resource adequacy.)

The legacy utilities are not in a position to acquire new renewables–they are forecasting falling loads and decreasing customers as CCAs grow. So the state cannot look to those utilities to meet California’s ambitious goals–it must incentivize CCAs with that task. The CCAs are already game, with many of them offering much more aggressive “green power” options to their customers than PG&E, SCE or SDG&E.

But CCAs place themselves at greater financial risk under the current rules if they sign more long-term contracts. If market prices fall, they must bear the risk of overpaying for both the legacy utility’s portfolio and their own.

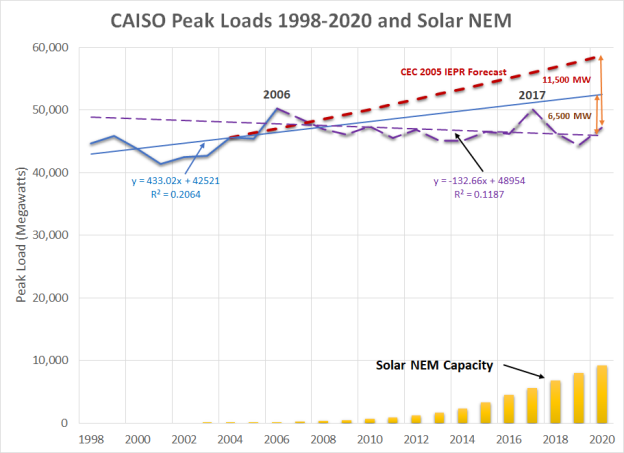

Solar net energy metered customers: Distributed solar generation installed under California’s net energy metering (NEM/NEMA) programs has mitigated and even eliminated load and demand growth in areas with established customers. This benefit supports protecting the investments that have been made by existing NEM/NEMA customers. Similarly, NEM/NEMA customers can displace investment in distribution assets. That distribution planners are not considering this impact appropriately is not an excuse for failing to value this benefit. For example, PG&E’s sales fell by 5% from 2010 to 2018 and other utilities had similar declines. Peak loads in the CAISO balancing authority reach their highest point in 2006 and the peak in August 2020 was 6% below that level.

Much of that decrease appears to have been driven by the installation of rooftop solar. The figure above illustrates the trends in CAISO peak loads in the set of top lines and the relationship to added NEM/NEMA installations in the lower corner. It also shows the CEC’s forecast from its 2005 Integrated Energy Policy Report as the top line. Prior to 2006, the CAISO peak was growing at annual rate of 0.97%; after 2006, peak loads have declined at a 0.28% trend. Over the same period, solar NEM capacity grew by over 9,200 megawatts. The correlation factor or “R-squared” between the decline in peak load after 2006 and the incremental NEM additions is 0.93, with 1.0 being perfect correlation. Based on these calculations, NEM capacity has deferred 6,500 megawatts of capacity additions over this period. Comparing the “extreme” 2020 peak to the average conditions load forecast from 2005, the load reduction is over 11,500 megawatts. The obvious conclusion is that these investments by NEM customers have saved all ratepayers both reliability and energy costs while delivering zero-carbon energy.

The CPUC now has before it a rulemaking in which the utilities and some ratepayer advocates are proposing to not only radically reduce the compensation to new NEM/NEMA customers but also to change the terms of the agreements for existing ones.

One of the key principles of providing financial stability is setting prices and rates for long-lived assets such as solar panels and generation plants at the economic value when the investment decision was made to reflect the full value of the assets that would have been acquired otherwise. If that new resource had not been built, either a ratebased generation asset would have been constructed by the utility at a cost that would have been recovered over a standard 30-year period or more likely, additional PPAs would have been signed. Additionally, the utilities’ investments and procurement costs are not subject to retroactive ratemaking under the rule prohibiting such ratemaking and Public Utilities Code Section 728, thus protecting shareholders from any risk of future changes in state or Commission policies.

Utility customers who similarly invest in generation should be afforded at least the same assurances as the utilities with respect to protection from future Commission decisions that may diminish the value of those investments. Moreover, customers do not have the additional assurances of achieving a certain net income so they already face higher risks than utility shareholders for their investments.

Generators are almost universally afforded the ability to recover capital investments based on prices set for multiple years, and often the economic life of their assets. Utilities are able to put investments in ratebase to be recovered at a fixed rate of return plus depreciation over several decades. Third-party generators are able to sign fixed price contracts for 10, 20, and even 40 years. Some merchant generators may choose to sell only into the short-term “hourly” market, but those plants are not committed to selling whenever the CAISO demands so. Generators are only required to do so when they sign a PPA with an assured payment toward investment recovery.

Ratepayers who make investments that benefit all ratepayers over the long term should be offered tariffs that provide a reasonable assurance of recovery of those investments, similar to the PPAs offered to generators. Ratepayers should be able to gain the same assurances as generators who sign long-term PPAs, or even utilities that ratebase their generation assets, that they will not be forced to bear all of the risk of investing of clean self-generation. These ratepayers should have some assurance over the 20-plus year expected life of their generation investment.

Severin Borenstein at the Energy Institure at Haas has plunged into the politics of devising policies for rooftop solar systems. I respond to two of his blog posts in two parts here, with Part 1 today. I’ll start by posting a link to my earlier blog post that addresses many of the assertions here in detail. And I respond to to several other additional issues here.

First, the claims of rooftop solar subsidies has two fallacious premises. First, it double counts the stranded cost charge from poor portfolio procurement and management I reference above and discussed at greater length in my blog post. Take out that cost and the “subsidy” falls substantially. The second is that solar hasn’t displaced load growth. In reality utility loads and peak demand have been flat since 2006 and even declining over the last three years. Even the peak last August was 3,000 MW below the record in 2017 which in turn was only a few hundred MW above the 2006 peak. Rooftop solar has been a significant contributor to this decline. Displaced load means displaced distribution investment and gas fired generation (even though the IOUs have justified several billion in added investment by forecasted “growth” that didn’t materialized.) I have documented those phantom load growth forecasts in testimony at the CPUC since 2009. The cost of service studies supposedly showing these subsidies assume a static world in which nothing has changed with the introduction of rooftop solar. Of course nothing could be further from the truth.

Second TURN and Cal Advocates have all be pushing against decentralization of the grid for decades back to restructuring. Decentralization means that the forums at the CPUC become less important and their influence declines. They have all fought against CCAs for the same reason. They’ve been fighting solar rooftops almost since its inception as well. Yet they have failed to push for the incentives enacted in AB57 for the IOUs to manage their portfolios or to control the exorbitant contract terms and overabundance of early renewable contracts signed by the IOUs that is the primary reason for the exorbitant growth in rates.

Finally, there are many self citations to studies and others with the claim that the authors have no financial interest. E3 has significant financial interests in studies paid for by utilities, including the California IOUs. While they do many good studies, they also have produced studies with certain key shadings of assumptions that support IOUs’ positions. As for studies from the CPUC, commissioners frequently direct the expected outcome of these. The results from the Customer Choice Green Book in 2018 is a case in point. The CPUC knows where it’s political interests are and acts to satisfy those interests. (I have personally witnessed this first hand while being in the room.) Unfortunately many of the academic studies I see on these cost allocation issues don’t accurately reflect the various financial and regulatory arrangements and have misleading or incorrect findings. This happens simply because academics aren’t involved in the “dirty” process of ratemaking and can’t know these things from a distance. (The best academic studies are those done by those who worked in the bowels of those agencies and then went to academics.)

We are at a point where we can start seeing the additional benefits of decentralized energy resources. The most important may be the resilience to be gained by integrating DERs with EVs to ride out local distribution outages (which are 15 times more likely to occur than generation and transmission outages) once the utilities agree to enable this technology that already exists. Another may be the erosion of the political power wielded by large centralized corporate interests. (There was a recent paper showing how increasing market concentration has led to large wealth transfers to corporate shareholders since 1980.) And this debate has highlighted the elephant in the room–how utility shareholders have escaped cost responsibility for decades which has led to our expensive, wasteful system. We need to be asking this fundamental question–where is the shareholders’ skin in this game? “Obligation to serve” isn’t a blank check.

Assembly Bill 1139 is offered as a supposed solution to unaffordable electricity rates for Californians. Unfortunately, the bill would undermine the state’s efforts to reduce greenhouse gas emissions by crippling several key initiatives that rely on wider deployment of rooftop solar and other distributed energy resources.

It will make complying with the Title 24 building code requiring solar panel on new houses prohibitively expensive. The new code pushes new houses to net zero electricity usage. AB 1139 would create a conflict with existing state laws and regulations.

The state’s initiative to increase housing and improve affordability will be dealt a blow if new homeowners have to pay for panels that won’t save them money.

It will make transportation electrification and the Governor’s executive order aiming for 100% new EVs by 2035 much more expensive because it will make it much less economic to use EVs for grid charging and will reduce the amount of direct solar panel charging.

Rooftop solar was installed as a long-term resource based on a contractual commitment by the utilities to maintain pricing terms for at least the life of the panels. Undermining that investment will undermine the incentive for consumers to participate in any state-directed conservation program to reduce energy or water use.

If the State Legislature wants to reduce ratepayer costs by revising contractual agreements, the more direct solution is to direct renegotiation of RPS PPAs. For PG&E, these contracts represent more than $1 billion a year in excess costs, which dwarfs any of the actual, if any, subsidies to NEM customers. The fact is that solar rooftops displaced the very expensive renewables that the IOUs signed, and probably led to a cancellation of auctions around 2015 that would have just further encumbered us.

The bill would force net energy metered (NEM) customers to pay twice for their power, once for the solar panels and again for the poor portfolio management decisions by the utilities. The utilities claim that $3 billion is being transferred from customers without solar to NEM customers. In SDG&E’s service territory, the claim is that the subsidy costs other ratepayers $230 per year, which translates to $1,438 per year for each NEM customer. But based on an average usage of 500 kWh per month, that implies each NEM customer is receiving a subsidy of $0.24/kWh compared to an average rate of $0.27 per kWh. In simple terms, SDG&E is claiming that rooftop solar saves almost nothing in avoided energy purchases and system investment. This contrasts with the presumption that energy efficiency improvements save utilities in avoided energy purchases and system investments. The math only works if one agrees with the utilities’ premise that they are entitled to sell power to serve an entire customer’s demand–in other words, solar rooftops shouldn’t exist.

Finally, this initiative would squash a key motivator that has driven enthusiasm in the public for growing environmental awareness. The message from the state would be that we can only rely on corporate America to solve our climate problems and that we can no longer take individual responsibility. That may be the biggest threat to achieving our climate management goals.

This report by Next10 and the University of California Energy Institute was prepared for the CPUC’s en banc hearing February 24. The report compares average electricity rates against other states, and against an estimate of “marginal costs”. (The latter estimate is too low but appears to rely mostly on the E3 Avoided Cost Calculator.) It shows those rates to be multiples of the marginal costs. (PG&E’s General Rate Case workpapers calculates that its rates are about double the marginal costs estimated in that proceeding.) The study attempts to list the reasons why the authors think these rates are too high, but it misses the real drivers on these rate increases. It also uses an incorrect method for calculating the market value of acquisitions and deferred investments, using the current market value instead of the value at the time that the decisions were made.

We can explore the reasons why PG&E’s rates are so high, much of which is applicable to the other two utilities as well. Starting with generation costs, PG&E’s portfolio mismanagement is not explained away with a simple assertion that the utility bought when prices were higher. In fact, PG&E failed in several ways.

First, PG&E knew about the risk of customer exit as early as 2010 as revealed during the PCIA rulemaking hearings in 2018. PG&E continued to procure as though it would be serving its entire service area instead of planning for the rise of CCAs. Further PG&E also was told as early as 2010 (in my GRC testimony) that it was consistently forecasting too high, but it didn’t bother to correct thee error. Instead, service area load is basically at the save level that it was a decade ago.

Second, PG&E could have procured in stages rather than in two large rounds of request for offers (RFOs) which it finished by 2013. By 2011 PG&E should have realized that solar costs were dropping quickly (if they had read the CEC Cost of Generation Report that I managed) and that it should have rolled out the RFOs in a manner to take advantage of that improvement. Further, they could have signed PPAs for the minimum period under state law of 10 years rather than the industry standard 30 years. PG&E was managing its portfolio in the standard practice manner which was foolish in the face of what was occurring.

Third, PG&E failed to offer part of its portfolio for sale to CCAs as they departed until 2018. Instead, PG&E could have unloaded its expensive portfolio in stages starting in 2010. The ease of the recent RPS sales illustrates that PG&E’s claims about creditworthiness and other problems had no foundation.

I calculated the what the cost of PG&E’s mismanagement has been here. While SCE and SDG&E have not faced the same degree of exit by CCAs, the same basic problems exist in their portfolios.

Another factor for PG&E is the fact that ratepayers have paid twice for Diablo Canyon. I explain here how PG&E fully recovered its initial investment costs by 1998, but as part of restructuring got to roll most of its costs back into rates. Fortunately these units retire by 2025 and rates will go down substantially as a result.

In distribution costs, both PG&E and SCE requested over $2 billion for “new growth” in each of its GRCs since 2009, despite my testimony showing that growth was not going to materialize, and did not materialize. If the growth was arising from the addition of new developments, the developers and new customers should have been paying for those additions through the line extension rules that assign that cost responsibility. The utilities’ distribution planning process is opaque. When asked for the workpapers underlying the planning process, both PG&E and SCE responded that the entirety were contained in the Word tables in each of their testimonies. The growth projections had not been reconciled with the system load forecasts until this latest GRC, so the totals of the individual planning units exceeded the projected total system growth (which was too high as well when compared to both other internal growth projections and realized growth). The result is a gross overinvestment in distribution infrastructure with substantial overcapacity in many places.

For transmission, the true incremental cost has not been fully reported which means that other cost-effective solutions, including smaller and closer renewables, have been ignored. Transmission rates have more than doubled over the last decade as a result.

The Next10 report does not appear to reflect the full value of public purpose program spending on energy efficiency, in large part because it uses a short-run estimate of marginal costs. The report similarly underestimates the value of behind-the-meter solar rooftops as well. The correct method for both is to use the market value of deferred resources–generation, transmission and distribution–when those resources were added. So for example, a solar rooftop installed in 2013 was displacing utility scale renewables that cost more than $100 per megawatt-hour. These should not be compared to the current market value of less than $60 per megawatt-hour because that investment was not made on a speculative basis–it was a contract based on embedded utility costs.

The California ISO Department of Market Monitoring notes in its comments to the CPUC on proposals to address resource adequacy shortages during last August’s rolling blackouts that the number of fixed price contracts are decreasing. In DMM’s opinion, this leaves California’s market exposed to the potential for greater market manipulation. The diminishing tolling agreements and longer term contracts DMM observes is the result of the structure of the power cost indifference adjustment (PCIA) or “exit fee” for departed community choice aggregation (CCA) and direct access (DA) customers. The IOUs are left shedding contracts as their loads fall.

The PCIA is pegged to short run market prices (even more so with the true up feature added in 2019.) The PCIA mechanism works as a price hedge against the short term market values for assets for CCAs and suppresses the incentives for long-term contracts. This discourages CCAs from signing long-term agreements with renewables.

The PCIA acts as an almost perfect hedge on the retail price for departed load customers because an increase in the CAISO and capacity market prices lead to a commensurate decrease in the PCIA, so the overall retail rate remains the same regardless of where the market moves. The IOUs are all so long on their resources, that market price variation has a relatively small impact on their overall rates.

This situation is almost identical to the relationship of the competition transition charge (CTC) implemented during restructuring starting in 1998. Again, energy service providers (ESPs) have little incentive to hedge their portfolios because the CTC was tied directly to the CAISO/PX prices, so the CTC moved inversely with market prices. Only when the CAISO prices exceeded the average cost of the IOUs’ portfolios did the high prices become a problem for ESPs and their customers.

As in 1998, the solution is to have a fixed, upfront exit fee paid by departing customers that is not tied to variations in future market prices. (Commissioner Jesse Knight’s proposal along this line was rejected by the other commissioners.) By doing so, load serving entities (LSEs) will be left to hedging their own portfolios on their own basis. That will lead to LSEs signing more long term agreements of various kinds.

The alternative of forcing CCAs and ESP to sign fixed price contracts under the current PCIA structure forces them to bear the risk burden of both departed and bundled customers, and the IOUs are able to pass through the risks of their long term agreements through the PCIA.

California would be well service by the DMM to point out this inherent structural problem. We should learn from our previous errors.

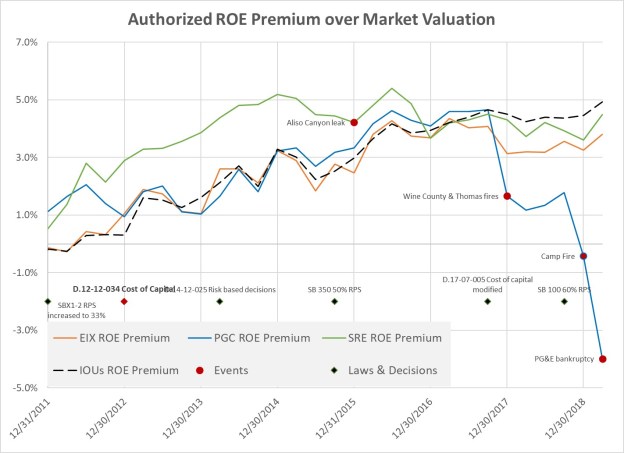

The wildfires that erupted in Sonoma County the night of October 8, 2017 signaled a manifest change not just limited to how we must manage risks, but even to the finances of our basic utility services. Forest fires had been distant events that, while expanding in size over the last several decades, had not impacted where people lived and worked. Southern California had experienced several large-scale fires, and the Oakland fire in 1991 had raced through a large city, but no one was truly ready for what happened that night, including Pacific Gas and Electric. Which is why the company eventually declared bankruptcy.

PG&E had already been punished for its poor management of its natural gas pipeline system after an explosion killed nine in San Bruno in 2010. The company was convicted in federal court, fined $3 million and placed on supervised probation under a judge.

PG&E also has extensive transmission and distribution network with more than 100,000 miles of wires. Over a quarter of that network runs through areas with significant wildfire risk. PG&E already had been charged with starting several forest fires, including the Butte fire in 2015, and its vegetation management program had been called out as inadequate by the California Public Utilities Commission (CPUC) since the 1990s. The CPUC caught PG&E diverting $495 million from maintenance spending to shareholders from 1992 to 1997; PG&E was fined $29 million. Meanwhile, two other utilities, Southern California Edison (SCE) and San Diego Gas and Electric (SDG&E) had instituted several management strategies to mitigate wildfire risk (not entirely successful), including turning off “line reclosers” during high winds to avoid short circuits on broken lines that can spark fires. PG&E resisted such steps.

On that October night, when 12 fires erupted, PG&E’s equipment contributed to starting 11 of those, and indirectly at least to other. Over 100,000 acres burned, destroying almost 9,000 buildings and killing 44 people. It was the most destructive fire in history, costing over $14 billion.

But PG&E’s problems were not over. The next year in November 2018, an even bigger fire in Butte County, the Camp fire, caused by a failure of a PG&E transmission line. That one burned over 150,000 acres, killing 85, destroying the community of Paradise and costing $16 billion plus. PG&E now faced legal liabilities of over $30 billion, which exceeds PG&E’s invested capital in its system. PG&E was potentially upside down financially.

The State of California had passed Assembly Bill 1054 that provided a fund of $21 billion to cover excess wildfire costs to utilities (including SCE and SDG&E), but it only covered fires after 2018. The Wine Country and Camp fires were not included, so PG&E faced the question of how to pay for these looming costs. Plus PG&E had an additional problem—federal Judge William Alsup supervising its parole stepped in claiming that these fires were a violation of its parole conditions. The CPUC also launched investigations into PG&E’s safety management and potential restructuring of the firm. PG&E faced legal and regulatory consequences on multiple fronts.

PG&E Corp, the holding company, filed for Chapter 11 bankruptcy on January 14, 2019. PG&E had learned from its 2001 bankruptcy proceeding for its utility company subsidiary that moving its legal and regulatory issues into the federal bankruptcy court gave the company much more control over its fate than being in multiple forums. Bankruptcy law afforded the company the ability to force regulators to increase rates to cover the costs authorized through the bankruptcy. And PG&E suffered no real consequences with the 2001 bankruptcy as share prices returned, and even exceeded, pre-filing levels.

As the case progressed, several proposals, some included in legislative bills, were made to take control of PG&E from its shareholders, through a cooperative, a state-owned utility, or splitting it among municipalities. Governor Gavin Newsom even called on Warren Buffet to buy out PG&E. Several localities, including San Francisco, made separate offers to buy their jurisdictions’ grid. The Governor and CPUC made certain demands of PG&E to restructure its management and board of directors, to which PG&E responded in part. PG&E changed its chief executive officer, and its current CEO, Bill Johnson, will resign on June 30. The Governor holds some leverage because he must certify that PG&E has complied by June 30, 2020 with the requirements of Assembly Bill 1054 that authorizes the wildfire cost relief fund for the utilities.

Meanwhile, PG&E implemented a quick fix to its wildfire risk with “public safety power shutoffs” (PSPS), with its first test in October 2019, which did not fare well. PG&E was accused of being excessive in the number of customers (over 800,000) and duration and failing to coordinate adequately with local governments. A subsequent PSPS event went more smoothly, but still had significant problems. PG&E says that such PSPS events will continue for the next decade until it has sufficiently “hardened” its system to mitigate the fire risk. Such mitigation includes putting power lines underground, changing system configuration and installing “microgrids” that can be isolated and self sufficient for short durations. That program likely will cost tens of billions of dollars, potentially increasing rates as much as 50 percent. One question will be who should pay—all ratepayers or those who are being protected in rural areas?

PG&E negotiated several pieces of a settlement, coming to agreements with hedge-fund investors, debt holders, insurance companies that pay for wildfire losses by residents and businesses, and fire victims. The victims are to be paid with a mix of cash and stock, with a face value of $13.5 billion; the victims are voting on whether to accept this agreement as this article is being written. Local governments will receive $1 billion, and insurance companies $11 billion, for a total of $24.5 billion in payouts. PG&E has lined up $20 billion in outside financing to cover these costs. The total package is expected to raise $58 billion.

The CPUC voted May 28 to approve PG&E’s bankruptcy plan, along with a proposed fine of $2 billion. PG&E would not be able to recover the costs for the 2017 and 2018 fires from ratepayers under the proposed order. The Governor has signaled that he is likely to also approve PG&E’s plan before the June 30 deadline.

PG&E is still asking for significant rate increases to both underwrite the AB 1054 wildfire protection fund and to implement various wildfire mitigation efforts. PG&E has asked for a $900 million interim rate increase for wildfire management efforts and a settlement agreement in its 2020 general rate case calls for another $575 million annual ongoing increase (with larger amounts to be added in the next three years). These amount to a more than 10 percent increase in rates for the coming year, on top of other rate increases for other investments.

Going forward, PG&E’s rates are likely to rise dramatically over the next five years to finance fixes to its system. Until that effort is effective, PSPS events will be widespread, maybe for a decade. On top of that is that electricity demand has dropped precipitously due to the coronavirus pandemic shelter in place orders, which is likely to translate into higher rates as costs are spread over a smaller amount of usage.

A catastrophic crisis calls for radical solutions that are considered out of the box. This includes asking utility shareholders to share in the the same pain as their customers.

M.Cubed is testifying on Southern California Edison’s 2021 General Rate Case (GRC) on behalf of the Small Business Utility Advocates. Small businesses represent nearly half of California’s economy. A recent survey shows that more than 40% of such firms are closed or will close in the near future. While these businesses struggle, the utilities currently assured a steady income, and SCE is asking for a 20% revenue requirement increase on top already high rates.

In this context, SBUA filed M.Cubed’s testimony on May 5 recommending that the California Public Utilities Commission take the following actions in response to SCE’s application related to commercial customers:

Order SCE to withdraw its present application and refile it with updated forecasts (that were filed last August) and assumptions that better fit the changed circumstances caused by the ongoing Covid-19 crisis.

Request that California issue a Rate Revenue Reduction bond that can be used to reduce SCE’s rates by 10%. The state did this in 1996 in anticipation of restructuring, and again in 2001 after the energy crisis.

Freeze all but essential utility investment. Much of SCE’s proposed increase is for “load growth” that has not materialized in the past, and even less likely now.

Require shareholders, rather than ratepayers, to bear the risks of underutilized or cost-ineffective investments.

Reduce Edison’s authorized rate-of-return by an amount proportionate to its lower sales until load levels and characteristics return to 2019 levels or demonstrably reach local demand levels at the circuit or substation that justify requested investment as “used and useful.”

Enact Covid-19 Commercial Class Economic Develop (ED) and Supply Chain Repatriation rates. These rates should be at least partially funded in part by SCE shareholders.

Order Edison to prioritize deployment of beneficial, flexible, distributed energy resources (DER) in-lieu of fixed distribution investments within its grid modernization program. SCE should not be throwing up barriers to this transformation.

Order Edison to reconcile its load forecasts for its local “adjustments” with its overall system forecast to avoid systemic over-forecasting, which leads to investment in excess distribution capacity.

Order SCE to revise and refile its distribution investment plan to align its load growth planning with the CPUC-adopted load forecasts for resource planning and to shift more funds to the grid modernization functions that focus on facilitating DER deployment specified in SCE’s application.

Order an audit of SCE’s spending in other categories to determine if the activities are justified and appropriate cost controls are in place. A comparison of authorized and actual 2019 capital expenditures found divergences as large as 65% from forecasted spending. The pattern shows that SCE appears to just spend up to its total authorized amount and then justify its spending after the fact.

M.Cubed goes into greater depth on the rationale for each of these recommendations. The CPUC does not offer many forums for these types of proposals, so SBUA has taken the opportunity offered by SCE’s overall revenue requirement request to plunge in.

TURN, the residential ratepayer intervenor group, submitted a comment letter to the California Public Utilities Commission (CPUC) in Pacific Gas and Electric’s (PG&E) bankruptcy investigation proceeding (I.19-09-016). TURN has some harsh statements asking for denial of recovery of some large expenses, including wildfire victim payments and legal fees. One particular passage caught my attention:

The stark truth is that PG&E is a recidivist felon that has caused multiple

major catastrophes within the space of a decade.

Recidivism is the act of a person repeating an undesirable behavior after they have either experienced negative consequences of that behavior, or have been trained to extinguish that behavior. It is also used to refer to the percentage of former prisoners who are rearrested for a similar offense.

But does “recidivist” apply in this situation for this reason: Has PG&E really suffered negative consequences from its previous behavior? So far, despite being convicted of felonies twice in the last decade, PG&E has been fined a total of $6.5 million for the San Bruno gas line explosion and the Camp Fire, which is equal to just over 4 hours of revenues for PG&E, and no one has gone to prison. PG&E continues to hold its franchise with few restrictions over most of northern California, and it appears headed for exiting bankruptcy by June 30 with a favorable finance plan in which current shareholders still hold most of the equity. It’s also not obvious how PG&E has been “trained” to extinguish its behavior, although the CPUC has instituted more oversight.

So, it’s not clear where and how PG&E has suffered significant negative consequences for its criminal acts, unless you consider “flea bites” as real punishment. To the contrary, PG&E has turned each of these events into money making enterprises. The first was by catching up on its deferred natural gas pipeline maintenance that it should have been spending on for decades. Instead, the CPUC could have simply ordered that the deferred spending be taken from past revenues. The second is the added investment of billions in hardening the rural distribution system and setting up back up generation in danger areas. That will add hundreds of millions or even a couple billion to annual revenues, all delivering a 10%+ return to company shareholders. Instead of negative consequences, PG&E has been able to turn these convictions into positive financial gains for its investors.